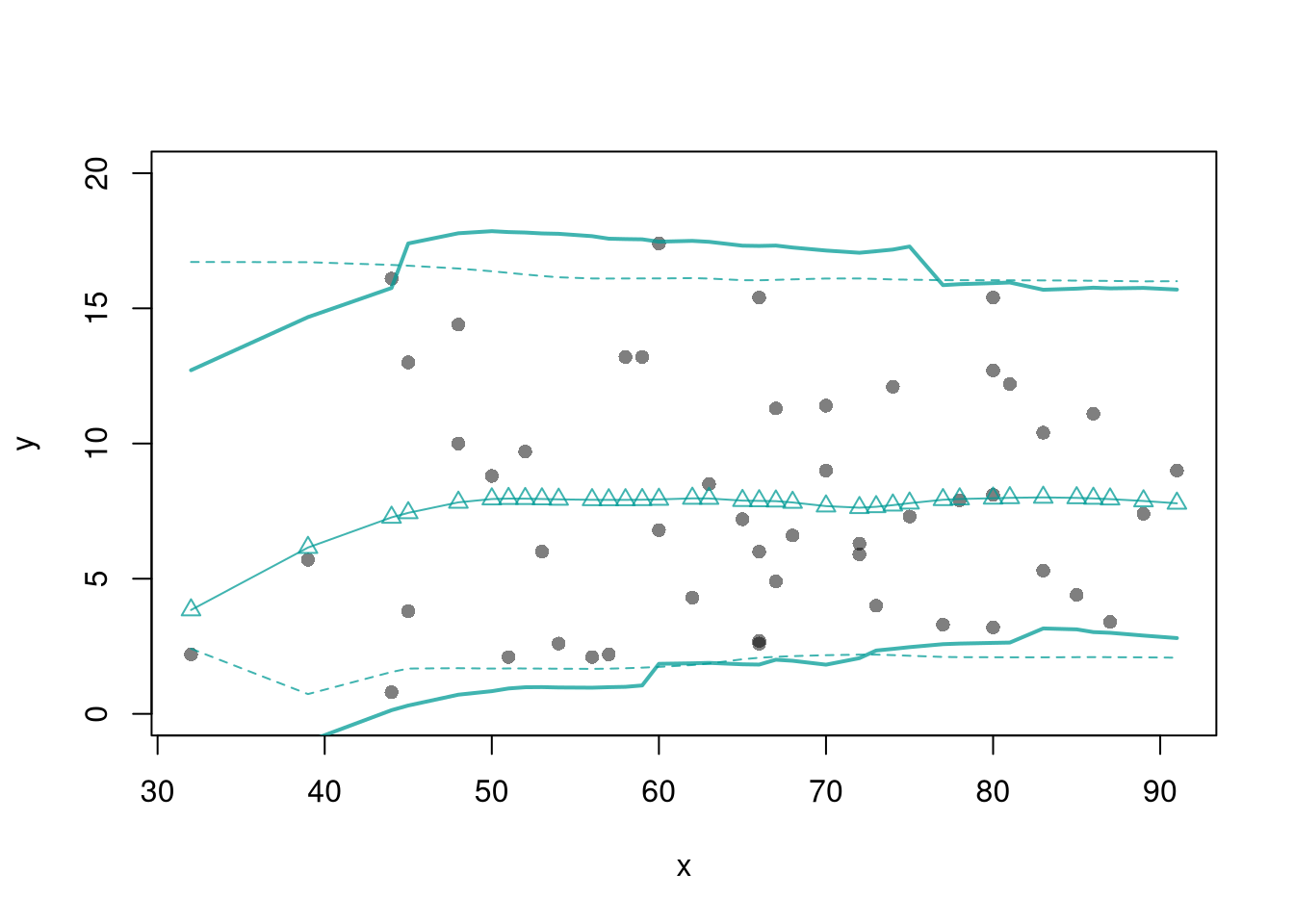

## Plot Simulated Data

x <- dat$x

x0 <- dat$x0

par(fig = c(0,1,0,1), new=F)

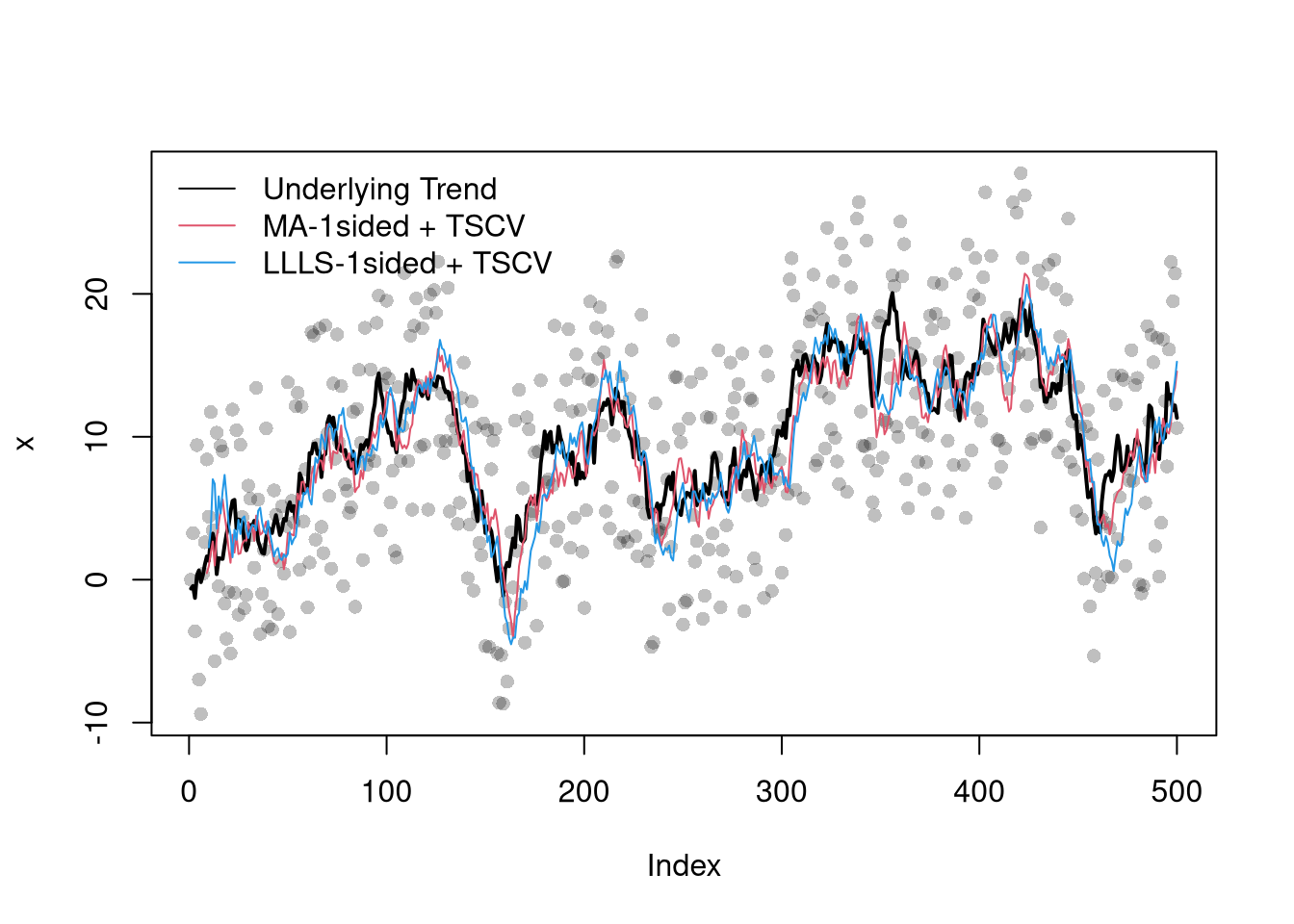

plot(x, pch=16, col=grey(0,.25))

lines(x0, col=1, lty=1, lwd=2)

## Work with differenced data?

#n <- length(Yt)

#plot(Yt[1:(n-1)], Yt[2:n],

# xlab='d Y (t-1)', ylab='d Y (t)',

# col=grey(0,.5), pch=16)

#Yt <- diff(Yt)

## TSCV One Sided Moving Average

filter_bws <- seq(1,20,by=1)

filter_mape_bws <- sapply(filter_bws, function(h){

bw <- c(0,rep(1/h,h)) ## Leave current one out

s2 <- filter(x, bw, sides=1)

pe <- s2 - x

mape <- mean( abs(pe)^2, na.rm=T)

})

filter_mape_star <- filter_mape_bws[which.min(filter_mape_bws)]

filter_h_star <- filter_bws[which.min(filter_mape_bws)]

filter_tscv <- filter(x, c(rep(1/filter_h_star,filter_h_star)), sides=1)

# Plot Optimization Results

#par(fig = c(0.07, 0.35, 0.07, 0.35), new=T)

#plot(filter_bws, filter_mape_bws, type='o', ylab='mape', pch=16)

#points(filter_h_star, filter_mape_star, pch=19, col=2, cex=1.5)

## TSCV for LLLS

library(np)

llls_bws <- seq(8,28,by=1)

llls_burnin <- 10

llls_mape_bws <- sapply(llls_bws, function(h){ # cat(h,'\n')

pe <- sapply(llls_burnin:nrow(dat), function(t_end){

dat_t <- dat[dat$t<t_end, ]

reg <- npreg(x~t, data=dat_t, bws=h,

ckertype='epanechnikov',

bandwidth.compute=F, regtype='ll')

edat <- dat[dat$t==t_end,]

pred <- predict(reg, newdata=edat)

pe <- edat$x - pred

return(pe)

})

mape <- mean( abs(pe)^2, na.rm=T)

})

llls_mape_star <- llls_mape_bws[which.min(llls_mape_bws)]

llls_h_star <- llls_bws[which.min(llls_mape_bws)]

#llls_tscv <- predict( npreg(x~t, data=dat, bws=llls_h_star,

# bandwidth.compute=F, regtype='ll', ckertype='epanechnikov'))

llls_tscv <- sapply(llls_burnin:nrow(dat), function(t_end, h=llls_h_star){

dat_t <- dat[dat$t<t_end, ]

reg <- npreg(x~t, data=dat_t, bws=h,

ckertype='epanechnikov',

bandwidth.compute=F, regtype='ll')

edat <- dat[dat$t==t_end,]

pred <- predict(reg, newdata=edat)

return(pred)

})

## Compare Fits Qualitatively

lines(filter_tscv, col=2, lty=1, lwd=1)

lines(llls_burnin:nrow(dat), llls_tscv, col=4, lty=1, lwd=1)

legend('topleft', lty=1, col=c(1,2,4), bty='n',

c('Underlying Trend', 'MA-1sided + TSCV', 'LLLS-1sided + TSCV'))