We will now dig a little deeper theoretically into the statistics we compute. When we know how the data are generated theoretically, we can often compute the theoretical value of the two most basic and often-used statistics: the mean and variance. This chapter draws a careful distinction between estimate, estimator, and parameter, then shows how the law of large numbers and the central limit theorem from the previous chapter follow from linearity of expectation and the \(1/n\) shrinkage of the variance.

Statistical Theory

Recall that we denote \(X_{i}\) as a random variable that can take on specific values \(x\) from the sample space with known probabilities (see this probability refresher if needed). For example, \(X_{i}\) is a coin that we will flip and it can land on heads (\(x=1\)) or tails (\(x=0\)).

- \(X_{i}\) is a random variable, taking on outcomes \(x\)

- \(\hat{X}_{i}\) is a realized value

Three closely related quantities are easily conflated: the fixed truth in the population, the formula we use to recover it, and the specific number that formula produces from one sample.

A population parameter (e.g., \(\mu\), \(\sigma^{2}\)) is a fixed but typically unknown number describing the population distribution.

An estimator (e.g., \(M\), \(V\)) is a random variable: a formula that computes a statistic on any sample of size \(n\) from the population.

An estimate (e.g., \(\hat{M}\), \(\hat{V}\)) is the specific number you get by applying the estimator to your particular sample.

The distinction is useful for being precise about uncertainty: a parameter has no sampling variability (it is just an unknown number), an estimator has a full sampling distribution, and an estimate is one realization from that distribution. For example, in flipping a coin three times, \(M = (X_{1}+X_{2}+X_{3})/3\) is the estimator computed on coins before they are flipped, and \(\hat{M}\) is the specific value after you flip them, and \(\mu\) is the theoretical value \(\frac{1}{2}0 + \frac{1}{2}1=1/2\).

Statistical definitions

| Estimate |

\(\hat{M}\), \(\hat{V}\) |

one number you compute for a single sample of size \(n\) |

empirical mean, variance |

sample mean, uncorrected sample variance (divide-by-\(n\)) |

|

| Estimator |

\(M\), \(V\) |

a random variable, formula that computes the statistic for any sample of size \(n\) |

|

|

|

| Population |

\(\mu\), \(\sigma^2\) |

a number defined by the theoretical distribution |

theoretical mean, variance |

population/long-run mean, variance |

|

For concreteness, we separately analyze how the theoretical mean and variance are computed for discrete and continuous random variables.

Population Parameters

Expected Value and Variance.

When we know the theoretical probabilities, the two most basic summaries (center and spread) can be computed exactly rather than estimated.

The expected value (or population mean) of a random variable \(X_{i}\), written \(\mathbb{E}[X_{i}]\) or \(\mu\), is the probability-weighted average of its values. For a discrete sample space, \(\mathbb{E}[X_{i}] = \sum_{x} x \cdot Prob(X_{i}=x)\); for continuous, it is the integral \(\int x f(x) dx\).

The population variance, written \(\mathbb{V}[X_{i}]\) or \(\sigma^{2}\), is the expected squared deviation from \(\mu\).

These population quantities are useful as targets: every sample-based estimator we built in earlier chapters is trying to recover one of them, and the gap between estimator and target is what sampling theory tries to control. The next two subsections show how to compute these for discrete and continuous random variables.

Discrete Random Variables.

If the sample space is discrete, we can compute the expected value, or theoretical mean, as \[\begin{eqnarray}

\mu = \mathbb{E}[X_{i}] = \sum_{x} x Prob(X_{i}=x),

\end{eqnarray}\] where \(\mathbb{E}\) is the expectation function that explicitly uses the population distribution via \(Prob(X_{i}=x)\): the probability the random variable \(X_{i}\) takes the particular value \(x\). Similarly, we can compute the population variance as \[\begin{eqnarray}

\sigma^2 = \mathbb{V}[X_{i}] = \mathbb{E}[(X_{i}-\mu)^2] = \sum_{x} \left(x - \mu \right)^2 Prob(X_{i}=x),

\end{eqnarray}\] where \(\mathbb{V}\) is the variance function which also explicitly uses the population distribution. The population standard deviation is \(\sigma = \sqrt{\mathbb{V}[X_{i}]}\), which measures the spread of the distribution of individual outcomes around the theoretical mean.

For example, consider a five-sided die with equal probability of landing on each side. I.e., \(X_{i}\) is a Discrete Uniform random variable with outcomes \(x \in \{1,2,3,4,5\}\). What is the theoretical mean? What is the variance and standard deviation? \[\begin{eqnarray}

\mu &=& \mathbb{E}[X_{i}] = 1\frac{1}{5} + 2\frac{1}{5} + 3\frac{1}{5} + 4\frac{1}{5} + 5\frac{1}{5} = 15/5 = 3\\

\sigma^2 = \mathbb{V}[X_{i}] &=& (1-3)^2\frac{1}{5} +

(2 - 3)^2\frac{1}{5} +

(3 - 3)^2\frac{1}{5} +

(4 - 3)^2\frac{1}{5} +

(5 - 3)^2\frac{1}{5} \\

&=& 2^2 \frac{1}{5} + 1^2\frac{1}{5} + 0^2 \frac{1}{5} + 1^2\frac{1}{5} + 2^2 \frac{1}{5}

= (4 + 1 + 1 + 4)/5 = 10/5 = 2\\

\sigma &=& \sqrt{2}

\end{eqnarray}\]

Code

# Computerized Way to Compute Mean

x <- c(1, 2, 3, 4, 5)

x_probs <- c(1/5, 1/5, 1/5, 1/5, 1/5)

X_mean <- sum(x*x_probs)

X_mean

## [1] 3

# Computerized Way to Compute SD

Xvar <- sum((x-X_mean)^2*x_probs)

Xvar

## [1] 2

Xsd <- sqrt(Xvar)

Xsd

## [1] 1.414214

# Verified by simulation

Xsim <- sample(x, prob=x_probs,

size=10000, replace=TRUE)

mean(Xsim)

## [1] 3.0116

sd(Xsim)

## [1] 1.418896

For example, consider an unfair coin with a \(3/4\) probability of heads (\(x=1\)) and a \(1/4\) probability of tails (\(x=0\)) has a theoretical mean of \[\begin{eqnarray}

\mathbb{E}[X_{i}] = 0\frac{1}{4} + 1\frac{3}{4} = \frac{3}{4}

\end{eqnarray}\] and a theoretical variance of \[\begin{eqnarray}

\mathbb{V}[X_{i}] = [0 - \frac{3}{4}]^2 \frac{1}{4} + [1 - \frac{3}{4}]^2 \frac{3}{4}

= \frac{9}{64} + \frac{3}{64}

= \frac{12}{64}

= \frac{3}{16}.

\end{eqnarray}\] Verify both the mean and variance by simulation.

Code

# A simulation of many coin flips

x <- c(0, 1)

x_probs <- c(1/4, 3/4)

X <- sample(x, prob=x_probs, size=1000, replace=TRUE)

round( mean(X), 4)

## [1] 0.767

round( var(X), 4)

## [1] 0.1789

Consider a four-sided die with outcomes \(\{1,2,3,4\}\) and corresponding probabilities \(\{1/8, 2/8, 1/8, 4/8\}\). The mean is \[\begin{eqnarray}

\mathbb{E}[X_{i}] = 1 \frac{1}{8} + 2 \frac{2}{8} + 3 \frac{1}{8} + 4 \frac{4}{8} = 3.

\end{eqnarray}\] The variance is the probability-weighted average squared deviation from the mean, \[\begin{eqnarray}

\mathbb{V}[X_{i}] = (1-3)^2 \frac{1}{8} + (2-3)^2 \frac{2}{8} + (3-3)^2 \frac{1}{8} + (4-3)^2 \frac{4}{8} = \frac{4 + 2 + 0 + 4}{8} = \frac{10}{8} = 1.25.

\end{eqnarray}\]

Code

x <- c(1, 2, 3, 4)

x_probs <- c(1/8, 2/8, 1/8, 4/8)

X_mean <- sum(x * x_probs)

X_mean

## [1] 3

X_var <- sum((x - X_mean)^2 * x_probs)

X_var

## [1] 1.25

# Verify by simulation

X <- sample(x, prob=x_probs, size=10000, replace=TRUE)

round(mean(X), 2)

## [1] 3.01

round(var(X), 2)

## [1] 1.25

Consider an unfair coin with a \(p\) probability of heads (\(x=1\)) and a \(1-p\) probability of tails (\(x=0\)), where \(p\) is a parameter between \(0\) and \(1\). The theoretical mean is \[\begin{eqnarray}

\mathbb{E}[X_{i}] = 1[p] + 0[1-p] = p

\end{eqnarray}\] and the theoretical variance is \[\begin{eqnarray}

\mathbb{V}[X_{i}]

= [1 - p]^2 p + [0 - p]^2 [1-p] = [1 - p]^2 p + p^2 [1-p]

= [1-p]p\left( [1-p] + p\right) = [1-p] p.

\end{eqnarray}\] So the theoretical standard deviation is \(\sigma=\sqrt{[1-p] p}\).

Suppose \(X_{i}\) is a discrete random variable with this probability mass function: \[\begin{eqnarray}

X_{i} &=& \begin{cases}

-1 & \text{ with probability } \frac{1}{2 \lambda^2} \\

0 & \text{ with probability } 1-\frac{1}{\lambda^2} \\

+1 & \text{ with probability } \frac{1}{2\lambda^2}

\end{cases},

\end{eqnarray}\] where \(\lambda>0\) is a parameter. What is the theoretical standard deviation?

For a discrete uniform random variable with the sample space \(\{1,2,3,4,5\}\), calculate the theoretical median and IQR.

Law of the Unconscious Statistician (LOTUS).

We often care about a transformed quantity like \(X_{i}^{2}\) or \(\log(X_{i})\), and would prefer not to derive its full distribution from scratch just to take its expectation.

The Law of the Unconscious Statistician (LOTUS) gives the expected value of a function of a random variable without first deriving the distribution of that function. For discrete \(X_{i}\) and any function \(g\), \(\mathbb{E}[g(X_{i})] = \sum_{x} g(x) Prob(X_{i}=x)\); for continuous \(X_{i}\), replace the sum with an integral against \(f(x)\).

LOTUS is useful as a shortcut: instead of deriving the distribution of \(g(X_{i})\) and then summing \(y \cdot Prob(g(X_{i}) = y)\), we sum \(g(x) \cdot Prob(X_{i}=x)\) directly using the original distribution of \(X_{i}\). You have already seen the special case \(g(X_{i})=\left(X_{i}-\mathbb{E}[X_{i}]\right)^2\), which is the population variance.

Let \(X_{i}\) take values \(\{1,2,3\}\) with \[\begin{eqnarray}

Prob(X_{i}=1)=0.2,\quad Prob(X_{i}=2)=0.5,\quad Prob(X_{i}=3)=0.3.

\end{eqnarray}\] Let \(g(x)=x^2+1\). Then \(g(1)=1^2+1=2\), \(g(2)=2^2+1=5\), \(g(3)=3^2+1=10\).

Then, by LOTUS, \[\begin{eqnarray}

\mathbb E[g(X_{i})]=\sum_x g(x)Prob(X_{i}=x)

&=& g(1)\cdot 0.2 + g(2)\cdot 0.5 + g(3)\cdot 0.3 \\

&=& 2 \cdot 0.2 + 5 \cdot 0.5 + 10 \cdot 0.3 \\

&=& 0.4 + 2.5 + 3 = 5.9.

\end{eqnarray}\]

Code

x <- c(1, 2, 3)

x_probs <- c(0.2, 0.5, 0.3)

g <- function(x) x^2 + 1

sum(g(x) * x_probs)

## [1] 5.9

Code

g <- function(x) x^2 + 1

# A theoretical example

x <- c(1, 2, 3, 4)

x_probs <- c(1/4, 1/4, 1/4, 1/4)

sum(g(x) * x_probs)

## [1] 8.5

# A simulation example

X <- sample(x, prob=x_probs, size=1000, replace=TRUE)

mean(g(X))

## [1] 8.526

If \(X_{i}\) is a continuous random variable (a random variable with a continuous sample space) and \(g\) is a function, then \(\mathbb E[g(X_{i})] = \int_{-\infty}^{\infty} g(x)f(x) dx\).

Code

x <- rexp(5e5, rate = 1) # X ~ Exp(1)

mean(sqrt(x)) # LOTUS Simulation

## [1] 0.8869345

sqrt(pi) / 2 # Exact via LOTUS integral

## [1] 0.8862269

Continuous Random Variables.

Many continuous random variables are parameterized by their means and variances. For example, the exponential distribution has a rate parameter \(\lambda\), which corresponds to the theoretical mean \(1/\lambda\) and variance \(1/\lambda^2\). For another example, the two parameters of the normal distribution are \(\mu\) and \(\sigma^2\), which corresponds to the theoretical mean and variance.

Code

# Exponential Random Variable

X <- rexp(5000, 2)

m <- mean(X)

round(m, 2)

## [1] 0.49

# Normal Random Variable

X <- rnorm(5000, 1, 2)

round(mean(X), 2)

## [1] 1.01

round(var(X), 2)

## [1] 4.01

Advanced and Optional

If the sample space is continuous, we can compute the theoretical mean (or expected value) as \[\begin{eqnarray}

\mathbb{E}[X] = \int x f(x) d x,

\end{eqnarray}\] where \(f(x)\) is the probability density for the particular value \(x\). Note that this is not a probability; probabilities are areas under \(f\).

Similarly, we can compute the theoretical variance as \[\begin{eqnarray}

\mathbb{V}[X_{i}]= \int \left(x - \mathbb{E}[X_{i}] \right)^2 f(x) d x,

\end{eqnarray}\]

For example, consider a random variable with a continuous uniform distribution over \([-1, 1]\). In this case, \(f(x)=1/[1 - (-1)]=1/2\) for each \(x \in [-1, 1]\) and \[\begin{eqnarray}

\mathbb{E}[X_{i}] = \int_{-1}^{1} \frac{x}{2} d x = \int_{-1}^{0} \frac{x}{2} d x + \int_{0}^{1} \frac{x}{2} d x = 0

\end{eqnarray}\] and \[\begin{eqnarray}

\mathbb{V}[X_{i}]= \int_{-1}^{1} x^2 \frac{1}{2} d x = \frac{1}{2} \frac{x^3}{3}|_{-1}^{1} = \frac{1}{6}[1 - (-1)] = 2/6 =1/3

\end{eqnarray}\]

Code

X <- USArrests[, 'Murder']

round( mean(X), 4)

## [1] 7.788

round( var(X), 4)

## [1] 18.9705

Estimates

You can estimate probabilities with data. With discrete data there are a limited number of unique outcomes, and we can estimate the probability of each outcome as \[\begin{eqnarray}

\hat{p}_{x}=\sum_{i=1}^{n}\mathbf{1}\left( \hat{X}_{i}=x\right)/n,

\end{eqnarray}\] where \(x\) is one particular value of interest. We often estimate the probabilities for each unique outcome.

Suppose there is an experiment with three possible outcomes, \(\{A, B, C\}\). It was repeated \(50\) times and discovered that \(A\) occurred \(10\) times, \(B\) occurred \(13\) times, and \(C\) occurred \(27\) times. The estimated probability of each outcome is found via the bar plot \(\hat{p}_{A} = 10/50\), \(\hat{p}_{B} = 13/50\), \(\hat{p}_{C} = 27/50\). We can also estimate the “in” probabilities as \(\hat{Prob}(A \text{ or } B)=10/50+13/50=23/50\) and \(\hat{Prob}(B \text{ or } C)=13/50+27/50=40/50\), as well as the “out” probability as \(\hat{Prob}(A \text{ or } C)=10/50+27/50=37/50\).

Do these calculations with the computer.

Sometimes, you may have a dataset of values and probability weights. In any case, we can then estimate the population mean via \[\begin{eqnarray}

\hat{M} &=& \sum_{x} x \hat{p}_{x},

\end{eqnarray}\] which is equivalent to the sample mean.

Suppose we flipped a coin \(100\) times and found that \(76\) were heads and \(24\) were tails. The estimated probabilities are \(76/100\) for the outcome \(X_{i}=1\) and \(24/100\) for the outcome \(X_{i}=0\). We compute the mean as \(\hat{M}=1\times 0.76 + 0 \times 0.24 = 0.76\).

Note that we get the same number if we instead computed \(\sum_{i} \hat{X}_{i}/100 = [\sum_{i=1}^{24} 0/100 + \sum_{i=25}^{100} 1/100 = [100-24]/100 = 0.76.\)

Code

# Simulate the coin flips

X <- sample(c(0, 1), 100, prob=c(0.24, 0.76), replace=TRUE)

# Compute a sample estimate using probability weights

P <- table(X) #table of counts

p <- c(P)/length(X) #frequencies (must sum to 1)

x <- as.numeric(names(p)) #unique values

cbind(x, p)

## x p

## 0 0 0.29

## 1 1 0.71

# Sample Mean Estimate

X_mean <- sum(x*p)

X_mean

## [1] 0.71

mean(X)

## [1] 0.71

Try estimating the sample mean the two different ways for another random sample

Code

x <- c(0, 1, 2)

x_probs <- c(1/3, 1/3, 1/3)

X <- sample(x, prob=x_probs, 1000, replace=TRUE)

# First Way (Computerized)

mean(X)

## [1] 0.989

# Second Way (Explicit Calculations)

# start with a table of counts like the previous example

The weighting idea generalizes to other statistics. E.g., we can also estimate variance with probability weights

Here is a concrete example of a weighted variance, for a random variable with values \(\{1,2,3\}\) and probability weights \(\{0.2, 0.5, 0.3\}\).

Code

x <- c(1, 2, 3)

x_probs <- c(0.2, 0.5, 0.3)

mx <- sum(x * x_probs) # weighted mean

x_diff <- (x - mx)^2 # squared deviations

x_var <- sum(x_probs * x_diff) # weighted variance

x_var

## [1] 0.49

Try it yourself with different values and weights.

You can estimate means and variances for continuous random variables with weights, but here we have an additional approximation error due to binning by the histogram.

Code

# values and probabilities

h <- hist(X, plot=FALSE)

wt <- h[['counts']]/length(X)

xt <- h[['mids']]

# Weighted mean

X_mean <- sum(wt*xt)

X_mean

## [1] 0.9604

# Compare to 'mean(x)'

Try it yourself with

Estimators

Means.

The LLN says the sample mean concentrates on the population mean as \(n\) grows; we can derive this from a more basic rule about how expectations distribute over sums.

Linearity of expectation states that for any random variables \(X_{1}, X_{2}\) and constants \(a, b\), \[\mathbb{E}[a X_{1} + b X_{2}] = a \mathbb{E}[X_{1}] + b \mathbb{E}[X_{2}].\] This holds whether or not the variables are independent.

Linearity of expectation is useful because it lets us reason about the mean of any linear combination of random variables without computing a joint distribution. Applied to the sample mean estimator \(M = \sum_{i=1}^{n} X_{i}/n\), with the constants \(1/n\): \[\begin{eqnarray}

\mathbb{E}\left[M\right] = \mathbb{E}\left[ \sum_{i=1}^{n} X_{i}/n \right] = \sum_{i=1}^{n} \mathbb{E}[X_{i}]/n.

\end{eqnarray}\] Assuming each data point has an identical mean \(\mathbb{E}[X_{i}]=\mu\), the expected value of the sample average is the mean: \(\mathbb{E}\left[M\right] = \sum_{i=1}^{n} \mu/n = \mu\). For a detailed treatment, see here.

For example, consider a coin flip with Heads \(X_{i}=1\) having probability \(p\) and Tails \(X_{i}=0\) having probability \(1-p\). First notice that \(\mathbb{E}[X_{i}]=p\). Then notice we can first \[\begin{eqnarray}

\mathbb{E}[X_{1}+X_{2}]

&=& [1+1][p \times p] + [1+0][p \times (1-p)] + [0+1][(1-p) \times p] + [0+0][(1-p) \times (1-p)] \quad \text{``HH + HT + TH + TT''} \\

&=& [1][p \times p] + [1][p \times (1-p)] + [0][(1-p) \times p] + [0][(1-p) \times (1-p)] \quad \text{first outcomes times prob.} \\

&+& [1][p \times p] + [0][p \times (1-p)] + [1][(1-p) \times p] + [0][(1-p) \times (1-p)] \quad \text{+second outcomes times prob.} \\

&=& [1][p \times p] + [1][p \times (1-p)] + [1][p \times p] + [1][(1-p) \times p] \quad \text{drop zeros}\\

&=& 1p (p + [1-p]) + 1p (p + [1-p]) = p+p \quad \text{algebra}\\

&=& \mathbb{E}[X_{1}] + \mathbb{E}[X_{2}].

\end{eqnarray}\] The theoretical mean is \(\mathbb{E}[\frac{X_{1}+X_{2}}{2}]=\frac{p+p}{2}=p\).

Variances.

Another famous theoretical result in statistics is that if we have independent and identical data (i.e., that each random variable \(X_{i}\) has the same mean \(\mu\), same variance \(\sigma^2\), and is drawn without any dependence on the previous draws), then the standard error of the sample mean decreases by \(1/\sqrt{n}\). Intuitively, this follows from thinking of the variance as a type of mean (the mean squared deviation from \(\mu\)). \[\begin{eqnarray}

\mathbb{V}\left[ M \right]

&=& \mathbb{V}\left[ \frac{\sum_{i=1}^{n} X_{i}}{n} \right]

= \sum_{i=1}^{n} \mathbb{V}\left[\frac{X_{i}}{n}\right]

= \sum_{i=1}^{n} \frac{\sigma^2}{n^2}

= \sigma^2/n\\

SE\left(M\right) &=& \sqrt{\mathbb{V}\left[ M \right] } = \sqrt{\sigma^2/n} = \sigma/\sqrt{n}.

\end{eqnarray}\]

For example, if the population has \(\sigma=10\) and we draw samples of size \(n=4\), then \(\mathbb{V}[M]=\sigma^2/n=100/4=25\) and \(SE(M)=\sigma/\sqrt{n}=10/2=5\). Quadrupling the sample size to \(n=16\) halves the standard error to \(10/\sqrt{16}=2.5\).

Note that the standard deviation refers to the variability of individual observations (in either a sample or population), and is hence different from the standard error. To be clear,

Types of variability

| Standard deviation |

individual observations within a sample or population |

\(\hat{S}\) or \(\sigma\) |

| Standard error |

a statistic across samples |

\(SE(M)\) |

Nonetheless, the sample standard deviation can be used to estimate the standard error of the sample mean. Specifically, assume that the data are approximately i.i.d and approximate the population standard deviation, \(\sigma\), with the sample standard deviation, \(\hat{S}\); \[\begin{eqnarray}

SE(M) \approx \sigma/\sqrt{n} \approx \hat{S}/\sqrt{n}.

\end{eqnarray}\]

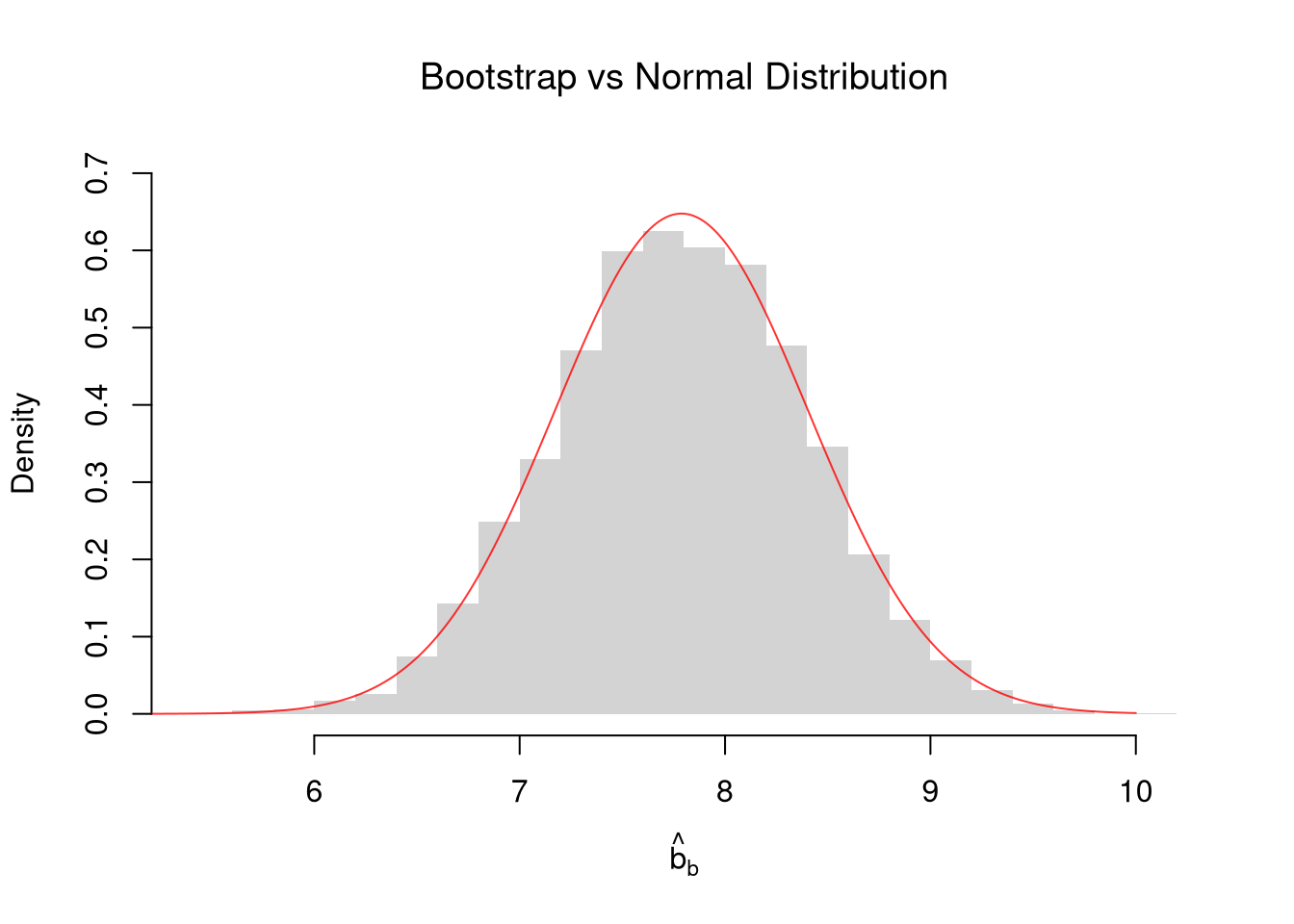

Another data-driven way is to create a bootstrap distribution for the sample mean and then compute the standard deviation of the bootstrap distribution \(\hat{SE}^{\text{boot}} \approx SE(M)\), as shown in Sampling & Resampling. The theory-driven estimate is often a little different from the bootstrap estimate, as the theory-driven estimate is based on idealistic assumptions (i.i.d. and normality) whereas the bootstrap estimate is driven by data that are often not ideal. The theory-driven estimate does have some advantages too, but we do not go into that as we would need more advanced mathematics.

Code

sample_dat <- USArrests[, 'Murder']

n <- length(sample_dat)

theory_se <- sd(sample_dat)/sqrt(n)

# Bootstrap estimates

bootstrap_means <- rep(NA, 9999)

for(b in seq_along(bootstrap_means)){

dat_id <- seq(1, n)

boot_id <- sample(dat_id , replace=TRUE)

dat_b <- sample_dat[boot_id] # c.f. jackknife

mean_b <- mean(dat_b)

bootstrap_means[b] <-mean_b

}

boot_se <- sd(bootstrap_means)

# Compare SE's

paste0('Bootstrap SE = ', round(boot_se, 3))

## [1] "Bootstrap SE = 0.613"

paste0('Class SE = ', round(theory_se, 3))

## [1] "Class SE = 0.616"

Shape.

Sometimes, the sampling distribution is approximately normal due to the CLT. With the sample mean \(M\) being approximately normal alongside i.i.d data, the distribution of \(M\) is approximately \(Normal(\mu, \hat{S}/\sqrt{n})\).

Code

# Bootstrap Distribution

hist(bootstrap_means, breaks=25,

main=NA, border=NA,

freq=FALSE, ylim=c(0, 0.7),

xlab=expression(hat(b)[b]))

title('Bootstrap vs Normal Distribution', font.main=1)

# Theoretical Distribution: Normal Approximation with IID SEs

x <- seq(5, 10, by=0.01)

fx <- dnorm(x, mean(sample_dat), theory_se)

lines(x, fx, col=rgb(1, 0, 0, .8), lty=1)

This normal approximation for the sampling distribution is the foundation for the confidence intervals we build in the next chapter.

Exercises

Comment the script you wrote for this chapter, then restart R and check that it runs from a clean session, then check the script with AI as explained in Working with AI. Write three sentences from memory on the main statistical idea of this chapter, and ask the assistant what is wrong, vague, or missing. Finish with your own questions about whatever you found hardest.

Explain in your own words the difference between an estimate \(\hat{M}\), an estimator \(M\), and a population parameter \(\mu\). Why is it important to distinguish between these three concepts?

Suppose \(X_{i}\) is a discrete random variable with outcomes \(\{1, 3, 5, 7\}\) and corresponding probabilities \(\{0.1, 0.2, 0.4, 0.3\}\). Compute the theoretical mean \(\mu\), variance \(\sigma^2\), and standard deviation \(\sigma\) by hand. Verify your answers using R.

Using the USArrests dataset in R, compute the sample mean and the bootstrap standard error of the mean for the Assault variable. Then compute the theory-driven standard error \(\hat{S}/\sqrt{n}\) and compare the two estimates.

Recall

This chapter formalized population parameters (\(\mu\), \(\sigma^{2}\)) and their estimators (\(M\), \(V\)), introduced LOTUS and linearity of expectation, and showed that the standard error of the sample mean shrinks at the \(1/\sqrt{n}\) rate. The five-sided die computation made the parameters concrete: with outcomes \(\{1, 2, 3, 4, 5\}\) each having probability \(1/5\), the population mean is \(\mu = 15/5 = 3\) and the variance is \(\sigma^{2} = (4+1+0+1+4)/5 = 2\). The \(1/\sqrt{n}\) rule then says that if a population has \(\sigma = 10\), samples of size \(n=4\) have \(SE(M) = 5\) but quadrupling the sample size to \(n=16\) halves the standard error to \(2.5\). In the next chapter we turn these results into confidence intervals: ranges of plausible values for the unknown parameter.