Code

# Simple random sample (no duplicates, equal probability)

x <- c(1, 2, 3, 4) # population

sample(x, 2, replace=FALSE) #sample

## [1] 3 1We rarely observe an entire population; instead we work with a sample and ask what its statistics tell us about the population that produced it. This chapter introduces sampling distributions (how a statistic varies from sample to sample), the two profound results that govern them (the Law of Large Numbers and the Central Limit Theorem), and the resampling tools (jackknife, bootstrap) that approximate sampling variability from a single dataset.

In practice we almost never observe the entire group we care about; we observe a slice and have to make judgments from that slice.

The simple random sample is useful as the default baseline: every other sampling scheme is described by how it departs from it, and the mathematical results in the rest of the chapter assume a simple random sample.

More generally, counting outcomes relies on a few rules. The multiplication rule says that if one choice has \(a\) options and an independent second choice has \(b\) options, then together they have \(a \times b\) options. When we select \(k\) items from \(n\) and the order matters, there are \(n \times (n-1) \times \cdots \times (n-k+1)\) permutations. When the order does not matter, we divide out the \(k!\) rearrangements and count \(\binom{n}{k}\) combinations.

Often, we think of the population as being infinitely large. This is an approximation that makes mathematical and computational work much simpler.

#All possible samples of two from a bag of numbers {1, 2, 3, 4} with replacement

#{1, 1} {1, 2} {1, 3}, {3, 4}

#{2, 2} {2, 3} {2, 4}

#{3, 3} {3, 4}

#{4, 4}

# Simple random sample (duplicates, equal probability)

sample(x, 2, replace=TRUE)

## [1] 4 3Intuition for infinite populations: imagine drawing names from a giant urn. If the urn has only \(10\) names, then removing one name slightly changes the composition of the urn, and the probabilities shift for the next name you draw. Now imagine the urn has \(100\) billion names, so that removing one makes no noticeable difference. We can pretend the composition never changes: each draw is essentially identical and independent (iid). We can actually guarantee the names are iid by putting any names drawn back into the urn (sampling with replacement).

A statistic computed on one sample is just one number; we want to know how much that number would change if we drew a different sample.

The sampling distribution is useful for quantifying uncertainty: its spread shows how much the statistic typically moves from sample to sample, and its center shows where it is targeted on average. For example, the sampling distribution of the mean shows how \(\hat{M}\) varies from sample to sample; it can also be called the probability distribution of the sample mean.

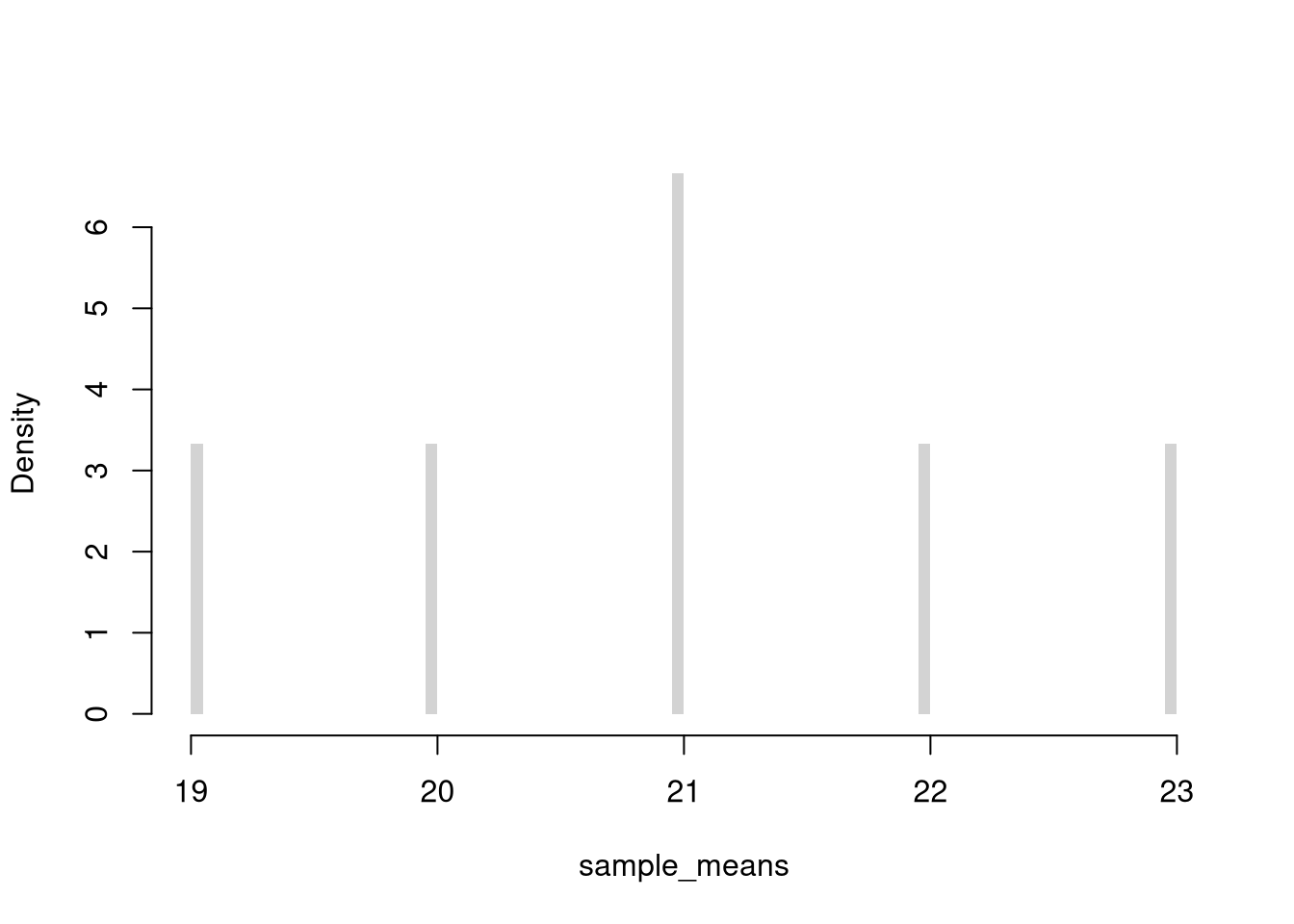

Given ages for population of \(4\) students, compute the sampling distribution for the mean with samples of \(n=2\).

X <- c(18, 20, 22, 24) # Ages for student population

# six possible samples

m1 <- mean( X[c(1, 2)] ) #{1, 2}

m2 <- mean( X[c(1, 3)] ) #{1, 3}

m3 <- mean( X[c(1, 4)] ) #{3, 4}

m4 <- mean( X[c(2, 3)] ) #{2, 3}

m5 <- mean( X[c(2, 4)] ) #{2, 4}

m6 <- mean( X[c(3, 4)] ) #{3, 4}

# sampling distribution

sample_means <- c(m1, m2, m3, m4, m5, m6)

hist(sample_means,

freq=FALSE, breaks=100,

main=NA, border=NA)

Now compute the sampling distribution for the median with samples of \(n=3\).

# Three Sample Example w/ Visual

par(mfrow=c(1, 3))

for(b in 1:3){

x <- runif(100)

m <- mean(x)

hist(x,

breaks=seq(0, 1, by=.1), #for comparability

freq=FALSE, main=NA, border=NA)

abline(v=m, col=rgb(1, 0, 0, .8), lwd=2)

title(paste0('mean= ', round(m, 2)), font.main=1)

}

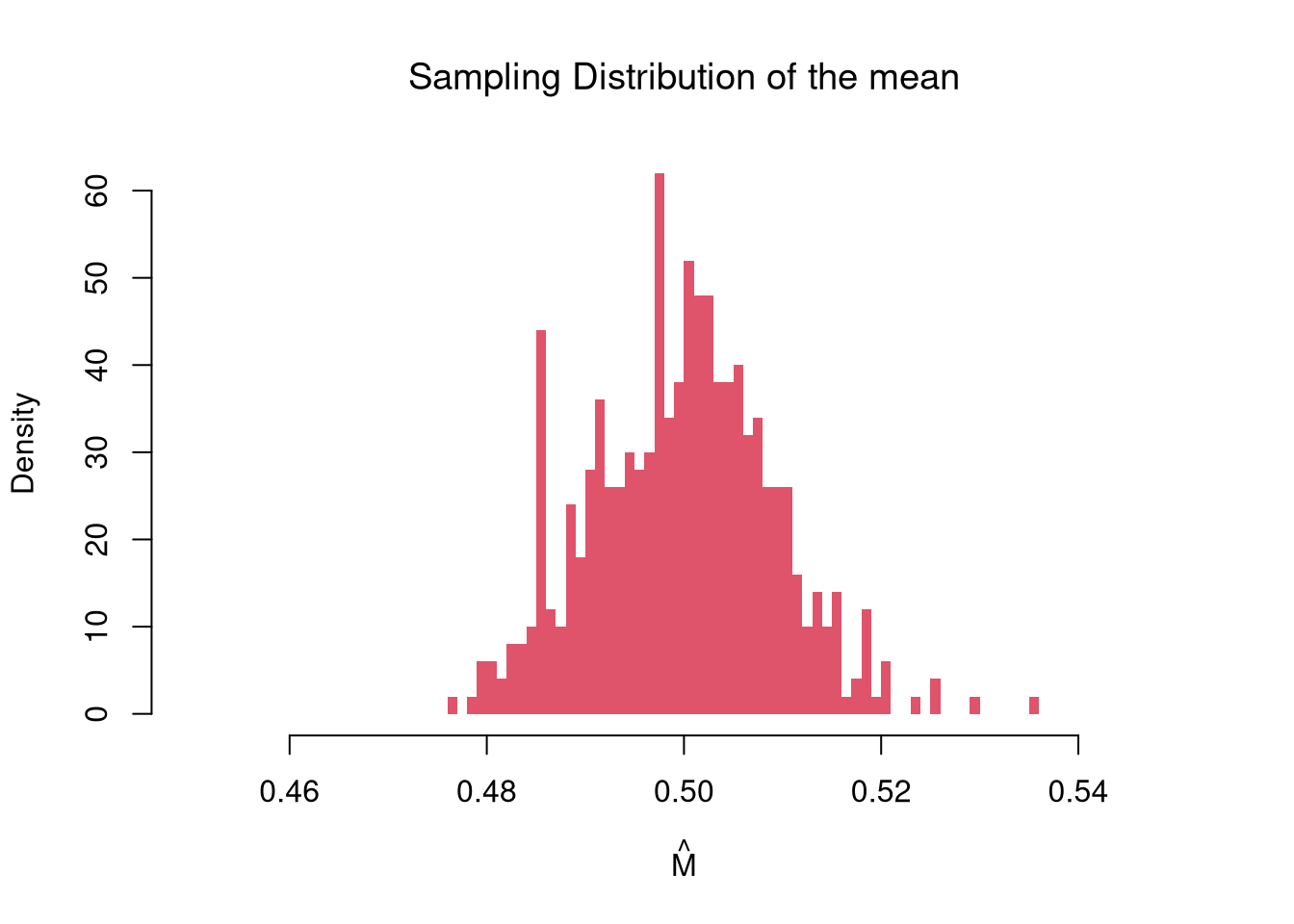

Examine the sampling distribution of the mean

# Many sample example

sample_means <- rep(NA, 500)

for(i in seq_along(sample_means)){

x <- runif(1000)

m <- mean(x)

sample_means[i] <- m

}

hist(sample_means,

breaks=seq(0.45, 0.55, by=.001),

border=NA, freq=FALSE,

col=rgb(1, 0, 0, .5),

xlab=expression(hat(M)),

main=NA)

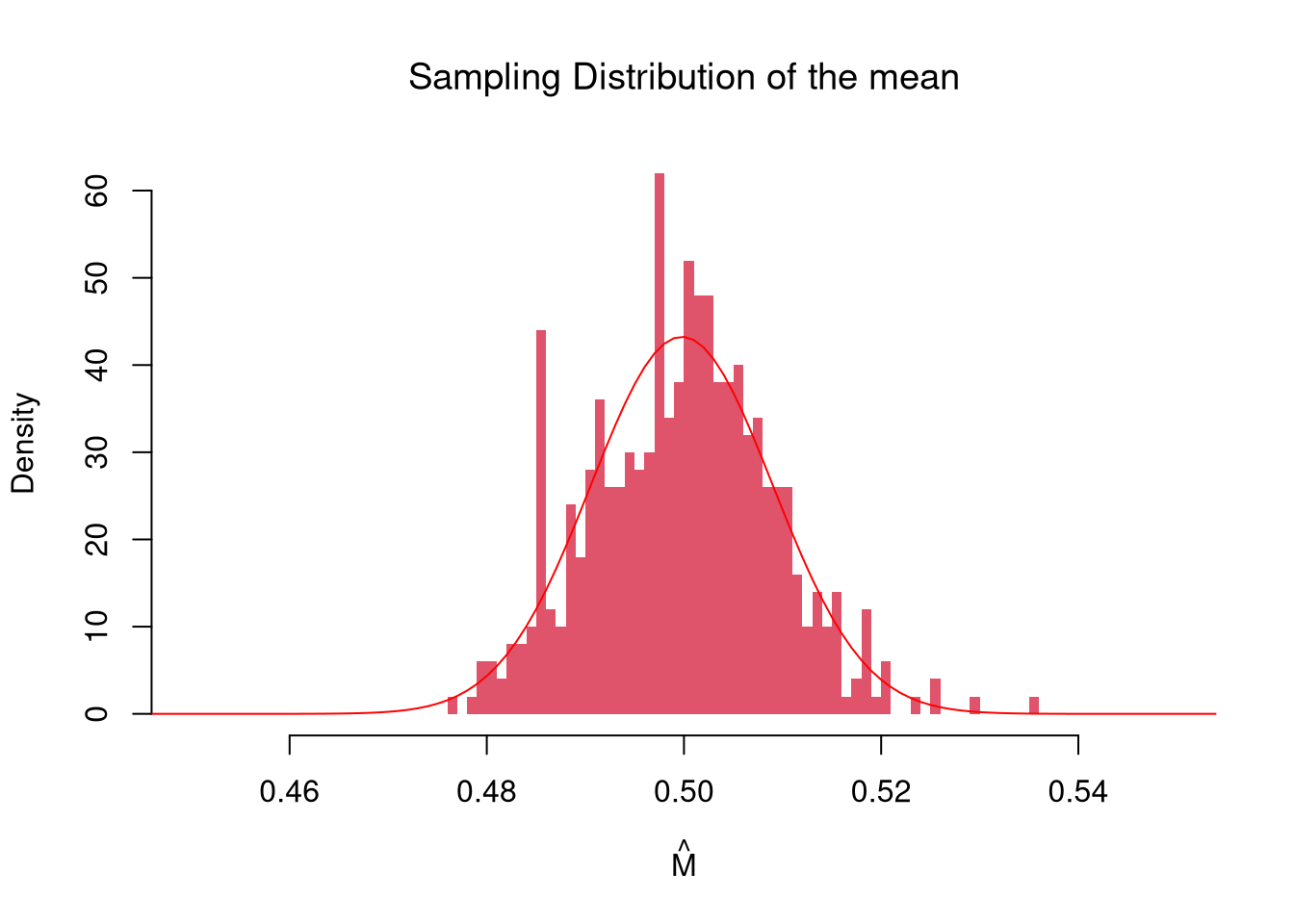

title('Sampling Distribution of the mean', font.main=1)

In this figure, you see two the most profound results known in statistics

The figure above suggests that the sample mean is centered on the true mean and gets less variable as \(n\) grows; the second of these observations is the Law of Large Numbers.

The LLN is useful as a guarantee that averaging works: even when individual observations are noisy, the sample mean of a large sample is close to the population mean. There are different variants of the theorem (weak vs. strong, with vs. without finite variance), but they all say some version of “the sample mean becomes more tightly centered around the true mean as we get more data”.

Notice where the sampling distribution is centered

m_LLLN <- mean(sample_means)

round(m_LLLN, 3)

## [1] 0.5and more tightly centered with more data

par(mfrow=c(1, 3))

for(n in c(5, 50, 500)){

sample_means_n <- rep(NA, 299)

for(i in seq_along(sample_means_n)){

x <- runif(n)

m <- mean(x)

sample_means_n[i] <- m

}

hist(sample_means_n,

breaks=seq(0, 1, by=.01),

border=NA, freq=FALSE,

col=rgb(1, 0, 0, .5),

xlab=expression(hat(M)),

main=NA)

title(paste0('n=', n), font.main=1)

}

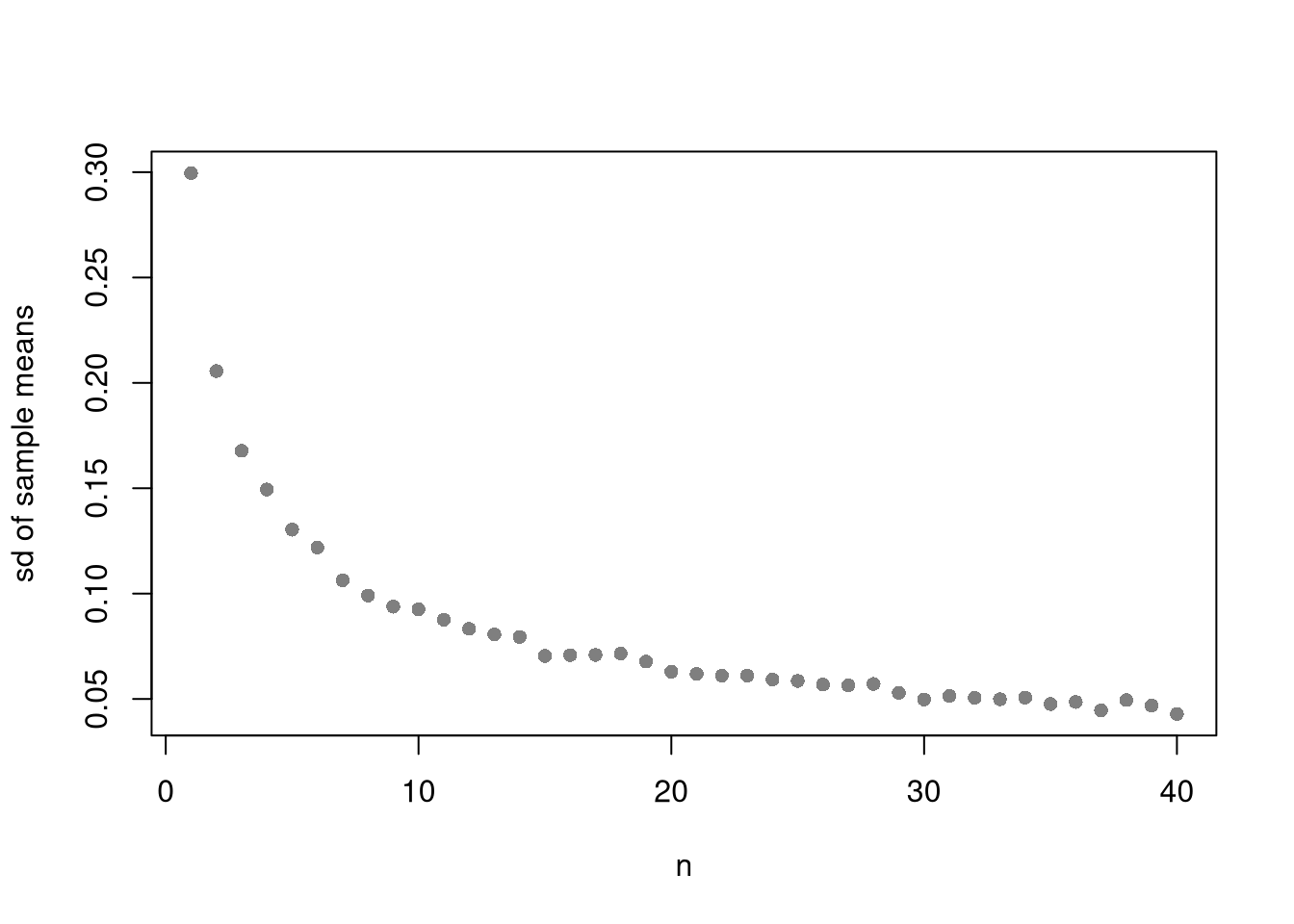

Plot the variability of the sample mean as a function of sample size

n_seq <- seq(1, 40)

sd_seq <- rep(NA, length(n_seq))

for(n in seq_along(sd_seq)){

sample_means_n <- rep(NA, 499)

for(i in seq_along(sample_means_n)){

x <- runif(n)

m <- mean(x)

sample_means_n[i] <- m

}

sd_seq[n] <- sd(sample_means_n)

}

plot(n_seq, sd_seq, pch=16, col=grey(0, 0.5),

xlab='n', ylab='sd of sample means', main=NA)

Here is the intuition for estimating the mean weight of an apple:

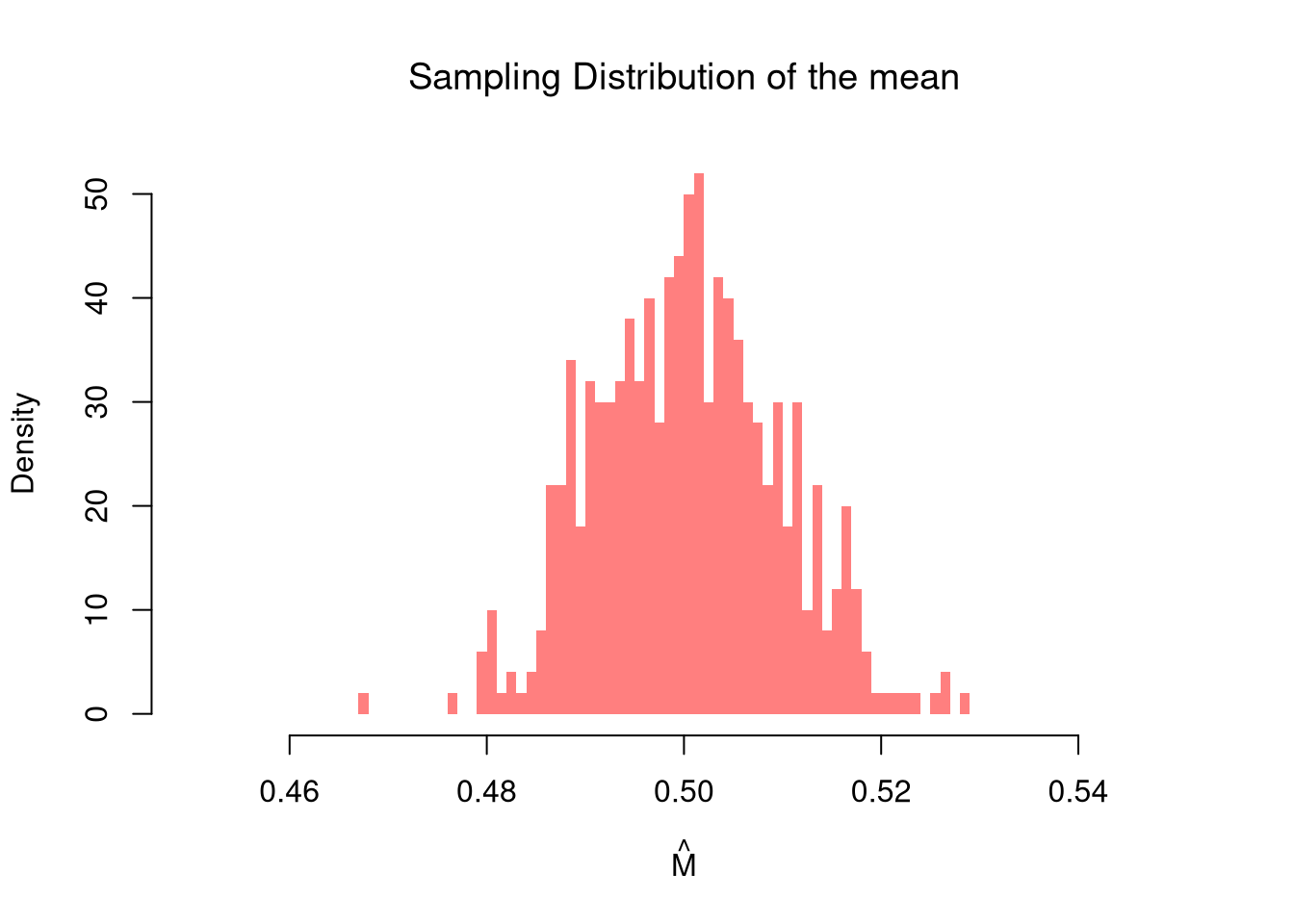

The LLN tells us the sampling distribution of \(\hat{M}\) tightens around the true mean; the next question is what shape it takes as it tightens.

The CLT is useful because it lets us treat sample means as approximately Normal even when we know little about the population distribution, which is why so many statistical procedures (intervals, hypothesis tests) are built on Normal calculations. There are different variants of the theorem, but all say some version of “the sampling distribution of the mean is approximately Normal”; the histogram shown above is one such example.

hist(sample_means,

breaks=seq(0.45, 0.55, by=.001),

border=NA, freq=FALSE,

col=rgb(1, 0, 0, .5),

xlab=expression(hat(M)),

main=NA)

title('Sampling Distribution of the mean', font.main=1)

# Approximately normal?

mu <- mean(sample_means)

mu_sd <- sd(sample_means)

x <- seq(0.1, 0.9, by=0.001)

fx <- dnorm(x, mu, mu_sd)

lines(x, fx, col=rgb(1, 0, 0, .8))

Many statistics have an approximately Normal sampling distribution.

For an example with another statistic, let’s the sampling distribution of the standard deviation.

# CLT example of the 'sd' statistic

sample_sds <- rep(NA, 1000)

for(i in seq_along(sample_sds)){

x <- runif(100) # same distribution

s <- sd(x) # different statistic

sample_sds[i] <- s

}

hist(sample_sds,

breaks=seq(0.2, 0.4, by=.01),

border=NA, freq=FALSE,

col=rgb(0, 0, 1, .5),

xlab=expression(hat(S)),

main=NA)

title('Sampling Distribution of the sd', font.main=1)

# Approximately normal?

mu <- mean(sample_sds)

mu_sd <- sd(sample_sds)

x <- seq(0.1, 0.9, by=0.001)

fx <- dnorm(x, mu, mu_sd)

lines(x, fx, col=rgb(0, 0, 1, .8))

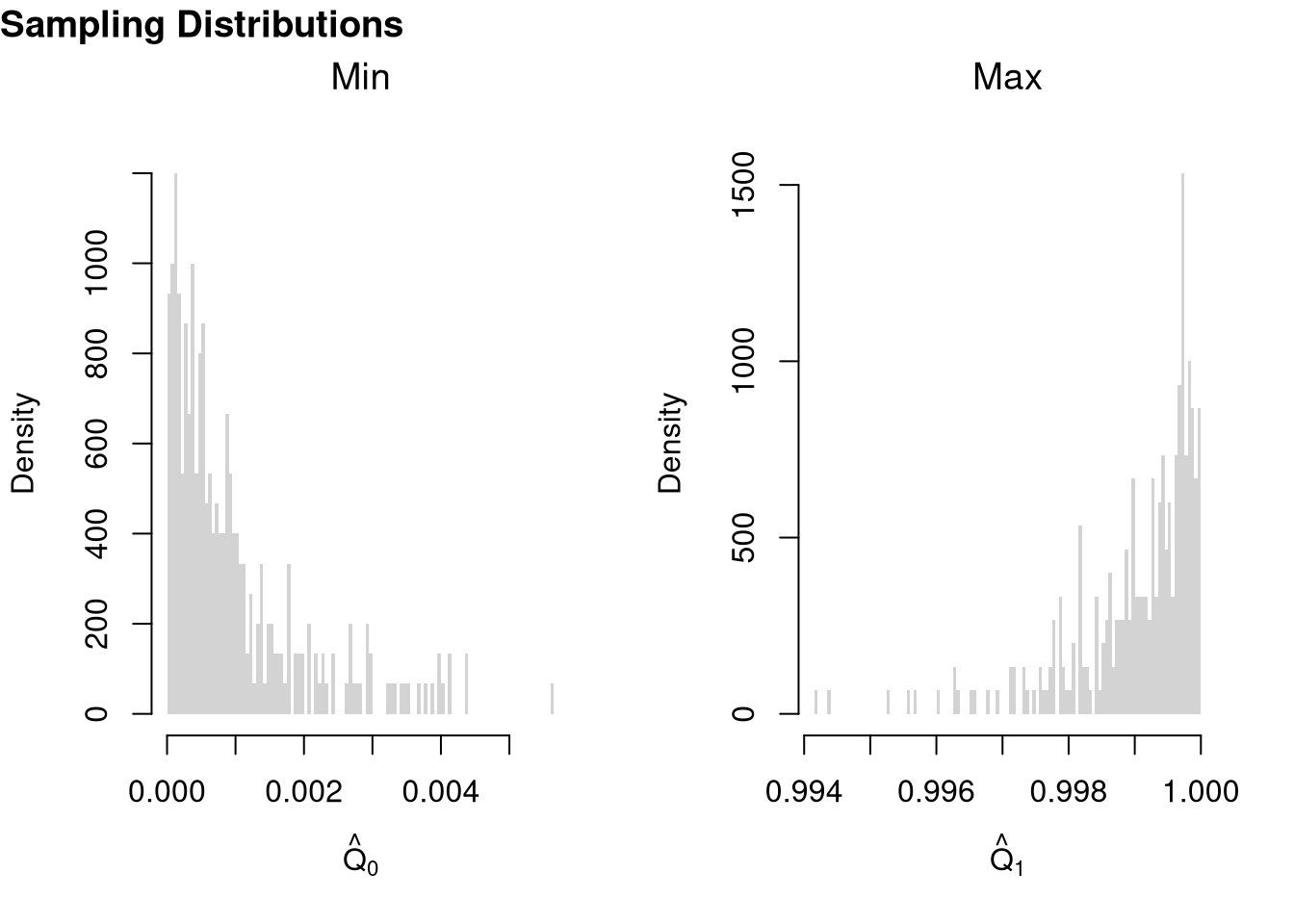

# try another random variable, such as rexp(100) instead of runif(100)It is beyond this class to prove this result mathematically, but you should know that not all sampling distributions are standard normal. The CLT approximation is better for “large \(n\)” datasets with “well behaved” variances. The CLT also does not apply to “extreme” statistics.

For example of “extreme” statistics, examine the sampling distribution of min and max statistics.

# Create 300 samples, each with 1000 random uniform variables

x_samples <- matrix(nrow=300, ncol=1000)

for(i in seq(1, nrow(x_samples))){

x_samples[i, ] <- runif(1000)

}

# Each row is a new sample

length(x_samples[1, ])

## [1] 1000

# Compute min and max for each sample

x_mins <- apply(x_samples, 1, quantile, probs=0)

x_maxs <- apply(x_samples, 1, quantile, probs=1)

# Plot the sampling distributions of min, median, and max

# Median looks normal. Maximum and minimum do not!

par(mfrow=c(1, 2))

hist(x_mins, breaks=100, main=NA,

xlab=expression(hat(Q)[0]), border=NA, freq=FALSE)

title('Min', font.main=1)

hist(x_maxs, breaks=100, main=NA,

xlab=expression(hat(Q)[1]), border=NA, freq=FALSE)

title('Max', font.main=1)

title('Sampling Distributions', outer=TRUE, line=-1, adj=0, font.main=1)

Explore another function, such as my_function <- function(x){ diff(range(x)) }

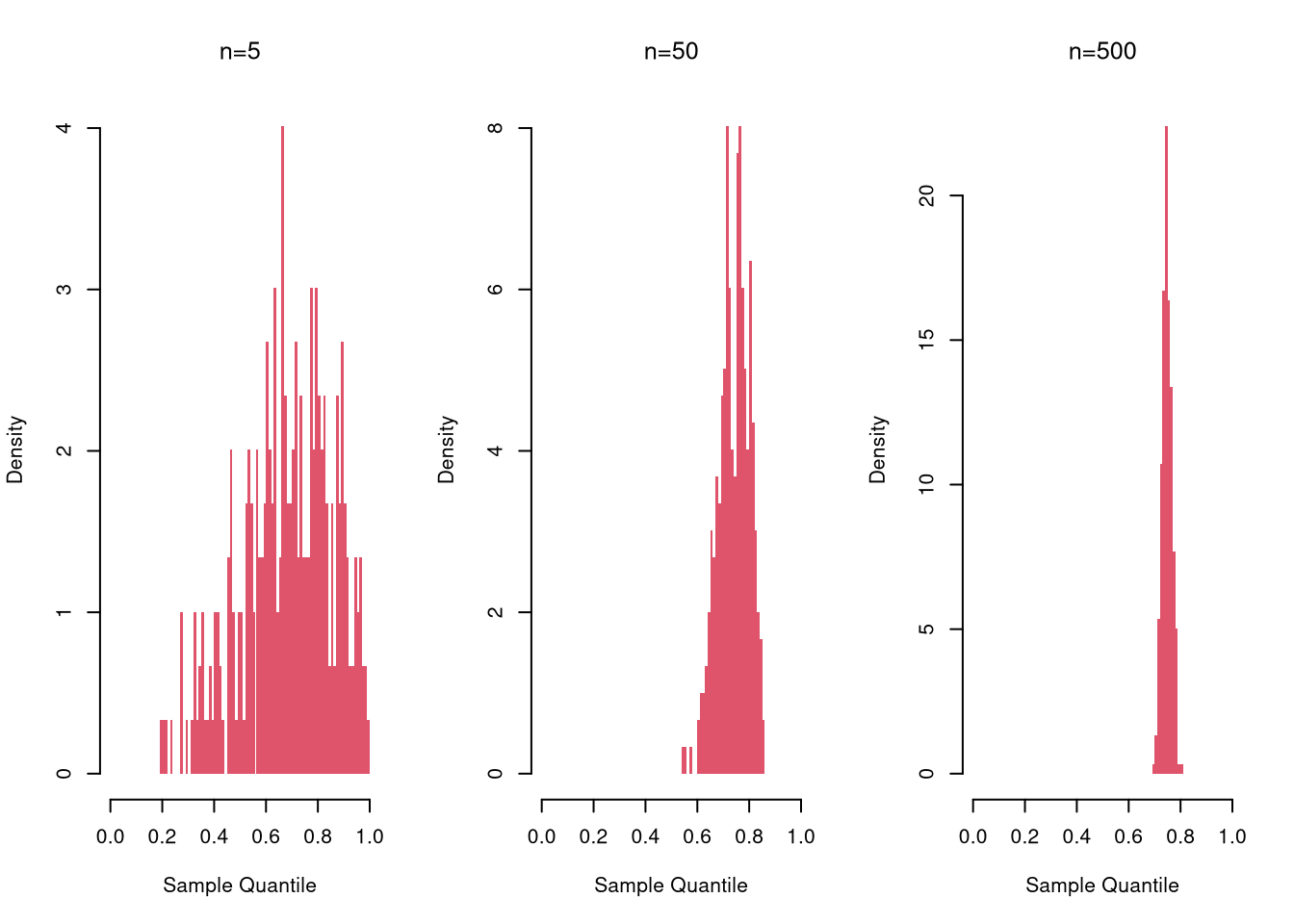

The Law of Large Numbers generalizes to many other statistics, like the median or sd from Numerical Statistics.1

Here is a sampling distribution for a quantile, for three different sample sizes

par(mfrow=c(1, 3))

for(n in c(5, 50, 500)){

sample_quants_n <- rep(NA, 299)

for(i in seq_along(sample_quants_n)){

x <- runif(n)

m <- quantile(x, probs=0.75) #upper quartile

sample_quants_n[i] <- m

}

hist(sample_quants_n,

breaks=seq(0, 1, by=.01),

border=NA, freq=FALSE,

col=rgb(1, 0, 0, .5),

xlab='Sample Quantile',

main=NA)

title(paste0('n=', n), font.main=1)

}

Here is a sampling distribution for a proportion, for three different sample sizes

par(mfrow=c(1, 3))

for(n in c(5, 50, 500)){

sample_props_n <- rep(NA, 299)

for(i in seq_along(sample_props_n)){

x <- sample(1:5, size=n, prob=c(1:5)/15, replace=TRUE)

p3 <- mean(x==3)

sample_props_n[i] <- p3

}

hist(sample_props_n,

breaks=seq(0, 1, by=.01),

border=NA, freq=FALSE,

col=rgb(1, 0, 0, .5),

xlab='Sample Proportion',

main=NA)

title(paste0('n=', n), font.main=1)

}

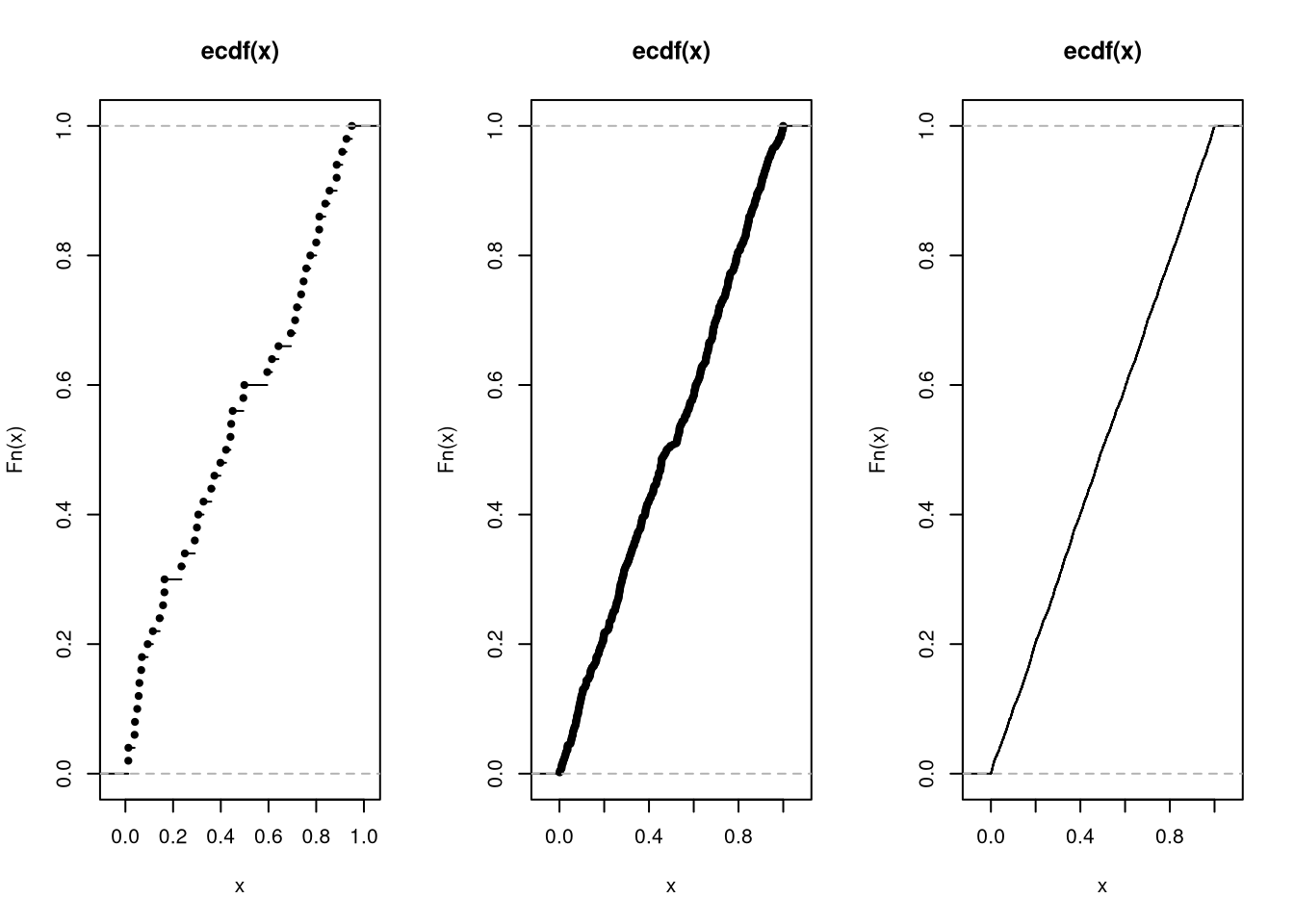

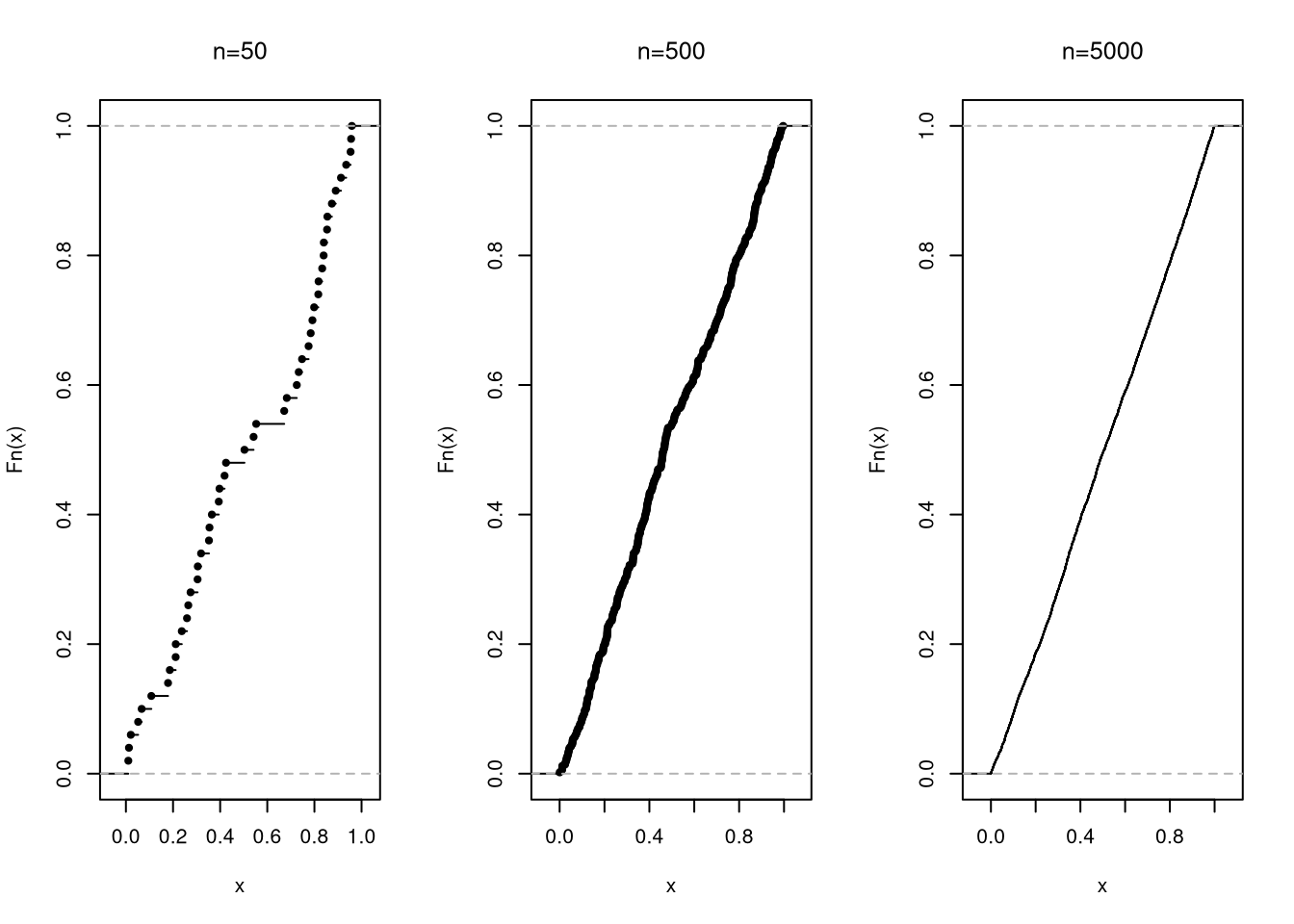

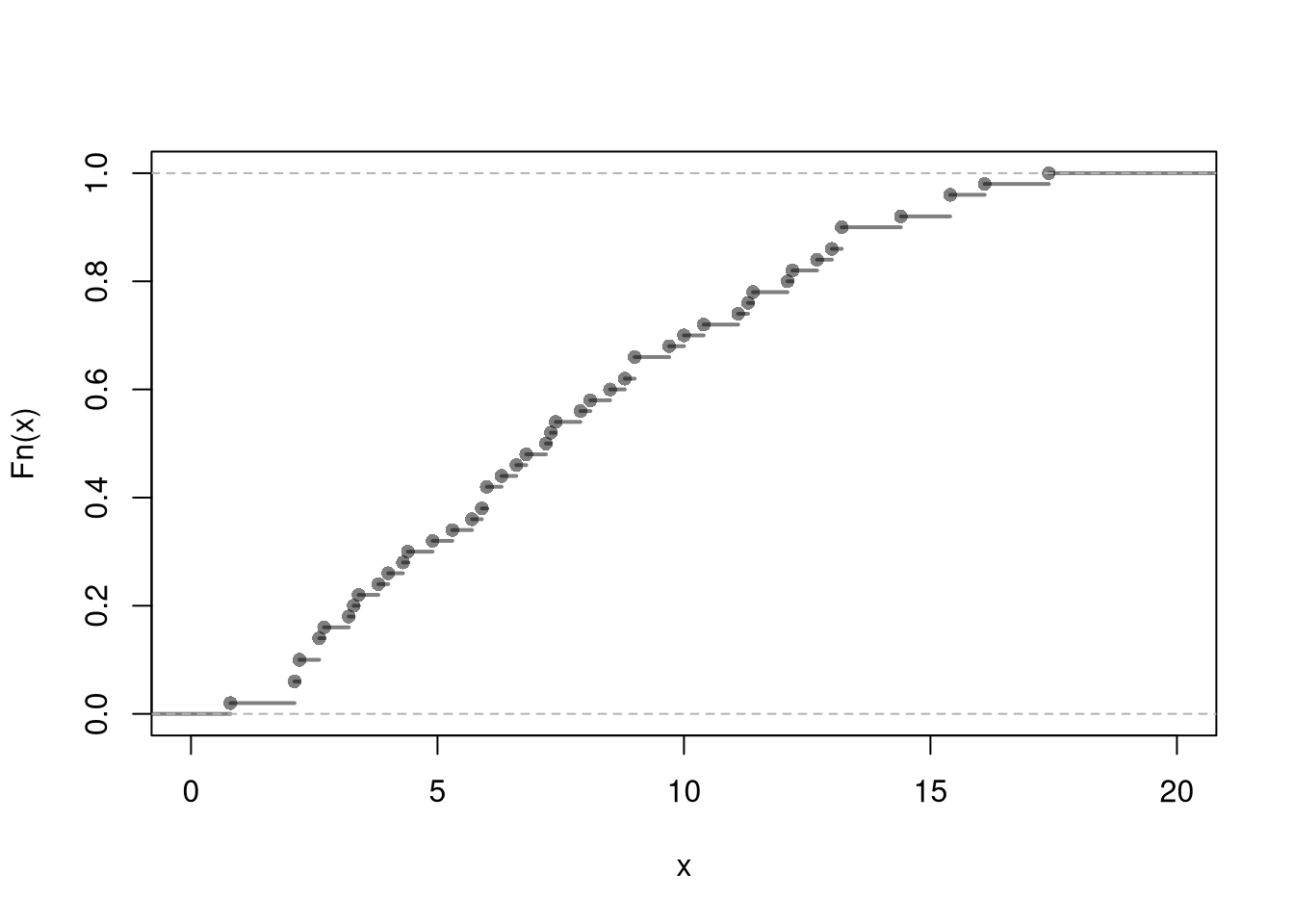

In fact, the Glivenko-Cantelli Theorem (GCT) shows entire empirical distribution converges: the ECDF gets increasingly close to the CDF as the sample sizes grow. This result is often termed the The Fundamental Theorem of Statistics.

par(mfrow = c(1, 3))

for (n in c(50, 500, 5000)) {

x <- runif(n)

Fx <- ecdf(x)

plot(Fx, main=NA)

title(paste0('n=', n), font.main=1)

}

Often, we only have one sample. How then can we estimate the sampling distribution of a statistic?

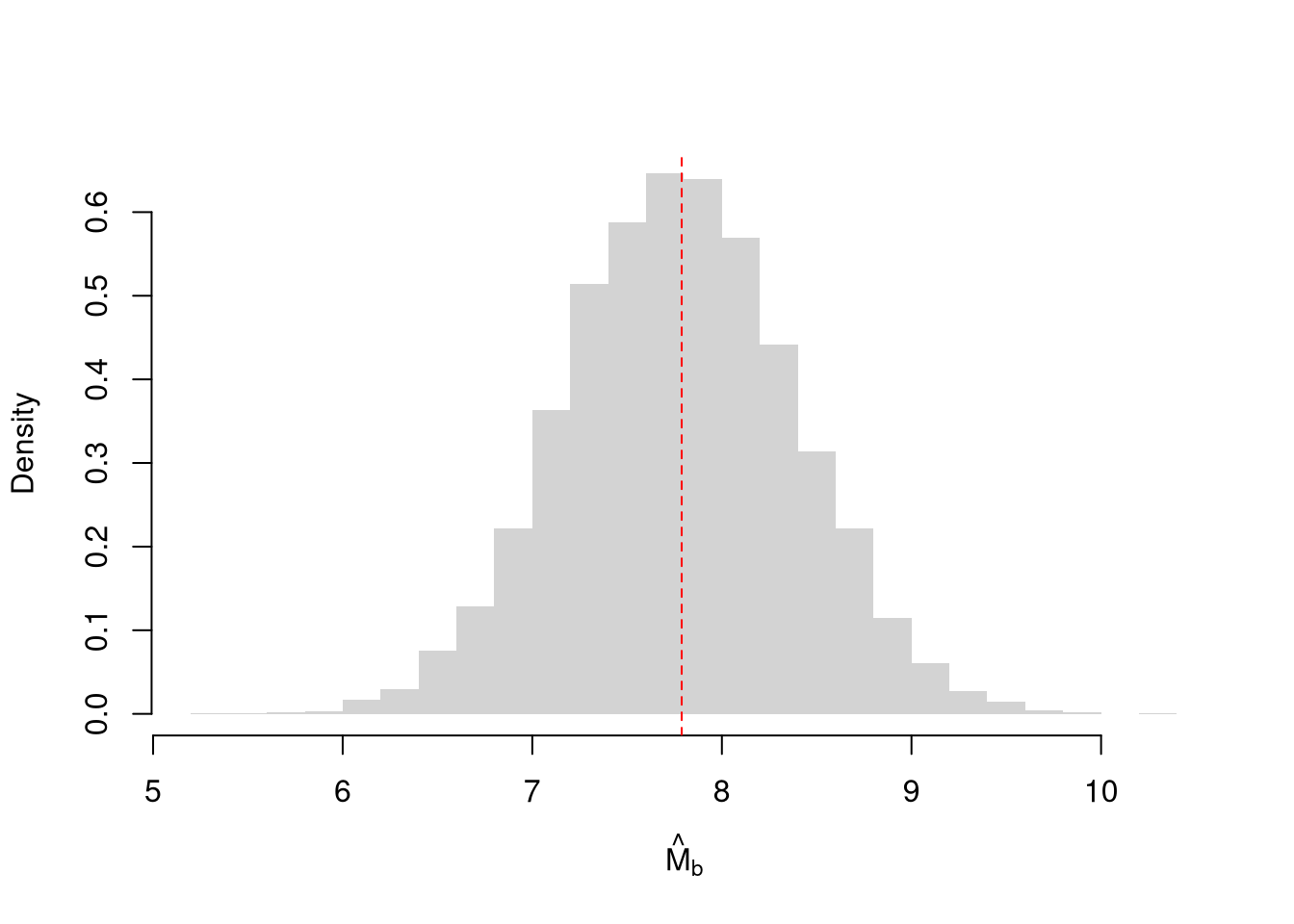

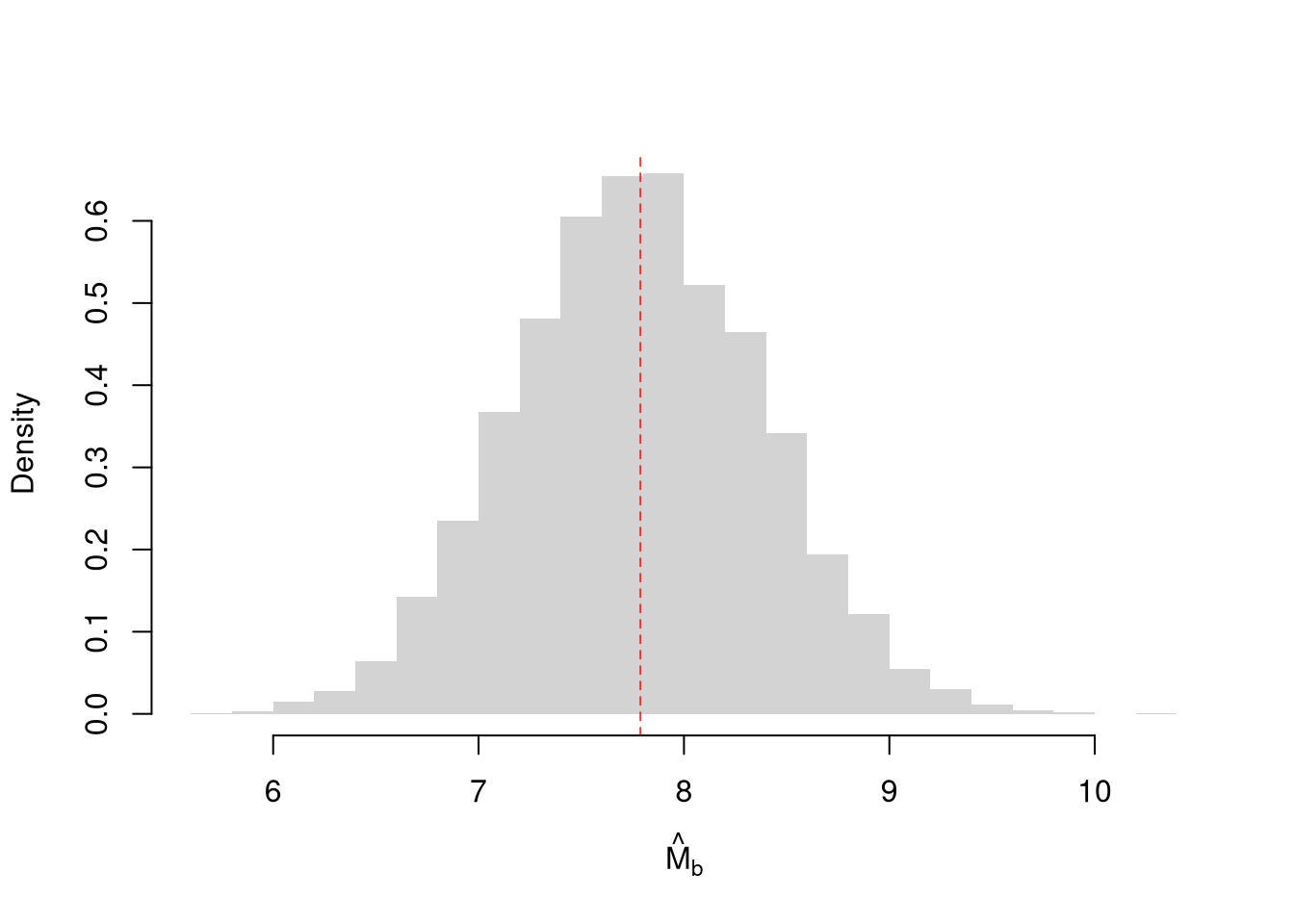

sample_dat <- USArrests[, 'Murder']

sample_mean <- mean(sample_dat)

sample_mean

## [1] 7.788We can resample our data. Hesterberg (2015) provides a nice illustration of the idea. The two most basic versions are the jackknife and the bootstrap, which are discussed below.

Note that we do not use the mean of the resampled statistics as a replacement for the original estimate. This is because the resampled distributions are centered at the observed statistic, not the population parameter. (The bootstrapped mean is centered at the sample mean, for example, not the population mean.) This means that we do not use resampling to improve on \(\hat{M}\). We use resampling to estimate sampling variability.

Here, we compute all “leave-one-out” estimates. Specifically, for a dataset with \(n\) observations, the jackknife uses \(n-1\) observations other than \(i\) for each unique subsample.

sample_dat <- USArrests[, 'Murder']

sample_mean <- mean(sample_dat)

# Jackknife Estimates

n <- length(sample_dat)

jackknife_means <- rep(NA, n)

for(i in seq_along(jackknife_means)){

dat_noti <- sample_dat[-i]

mean_noti <- mean(dat_noti)

jackknife_means[i] <- mean_noti

}

hist(jackknife_means, breaks=25,

border=NA, freq=FALSE,

main=NA, xlab=expression(hat(M)[-i]))

abline(v=sample_mean, col=rgb(1, 0, 0, .8), lty=2)

The jackknife uses only \(n\) leave-one-out subsamples, which tends to underestimate variability; a more flexible approach builds many resamples of full size \(n\) by allowing duplicates.

The bootstrap is useful when no closed-form expression for the sampling distribution is available (common for medians, quantiles, ratios, or any custom statistic), because the recipe is identical regardless of the statistic computed on each resample. Each bootstrap sample \(b=1\dots B\) produces one value of the statistic, and we typically repeat the resampling many times (e.g., \(B=9999\)) to estimate the sampling distribution.

# Bootstrap estimates

bootstrap_means <- rep(NA, 9999)

for(b in seq_along(bootstrap_means)){

boot_id <- sample(n, replace=TRUE)

dat_b <- sample_dat[boot_id] # c.f. jackknife

mean_b <- mean(dat_b)

bootstrap_means[b] <-mean_b

}

hist(bootstrap_means, breaks=25,

border=NA, freq=FALSE,

main=NA, xlab=expression(hat(M)[b]))

abline(v=sample_mean, col=rgb(1, 0, 0, .8), lty=2)

Why does this work? The sample: \(\{\hat{X}_{1}, \hat{X}_{2}, ... \hat{X}_{n}\}\) is drawn from a CDF \(F\). Each bootstrap sample: \(\{\hat{X}_{1}^{(b)}, \hat{X}_{2}^{(b)}, ... \hat{X}_{n}^{(b)}\}\) is drawn from the ECDF \(\hat{F}\). With \(\hat{F} \approx F\), each bootstrap sample is approximately a random sample. So when we compute a statistic on each bootstrap sample, we approximate the sampling distribution of the statistic.

Note that both Jackknife and Bootstrap resampling methods provide imperfect estimates, and can give different numbers.

Having an entire sampling distribution is conceptually clear but unwieldy in practice; we usually compress it to a single number describing its spread.

The standard error is useful for reporting how precise an estimate is in a single number: a small \(SE\) means the statistic would change little across samples, a large \(SE\) means it could swing widely. The two “standard” quantities are easy to confuse but answer different questions:

For a bootstrap example

Also note that each additional data point you have provides more information, which ultimately decreases the standard error of your estimates. This is why statisticians will often recommend that you to get more data. However, the improvement in the standard error increases at a diminishing rate. In economics, this is known as diminishing returns and why economists may recommend you do not get more data.

B <- 999 # number of bootstrap samples

Nseq <- seq(1, length(sample_dat), by=1) # different resample sizes

n_id <- seq_along(sample_dat) # who to potentially resample

## For each sample size, compute the bootstrap SE

SE <- rep(NA, length(Nseq))

for(n in seq_along(Nseq)){

sample_stats_n <- rep(NA, B)

for(b in seq(1, B)){

b_id <- sample(n_id, size=n, replace=TRUE)

x_b <- sample_dat[b_id]

x_stat_b <- mean(x_b) # statistic of interest

sample_stats_n[b] <- x_stat_b

}

se_n <- sd(sample_stats_n) # How much the statistic varies across samples

SE[n] <- se_n

}

plot(Nseq, SE, pch=16, col=grey(0, 0.5),

ylab='standard error', xlab='sample size', main=NA)

The above procedure works for many different statistics

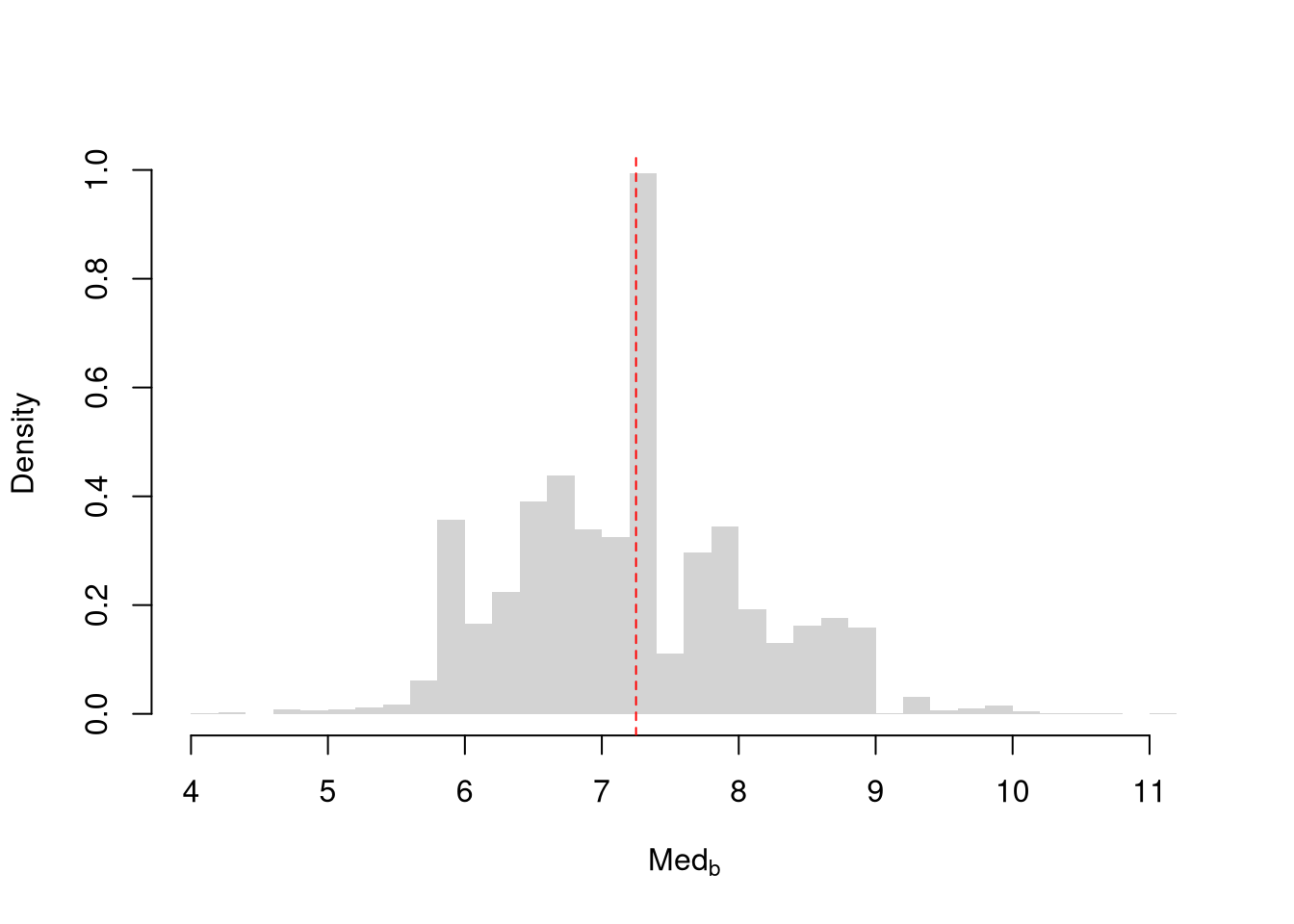

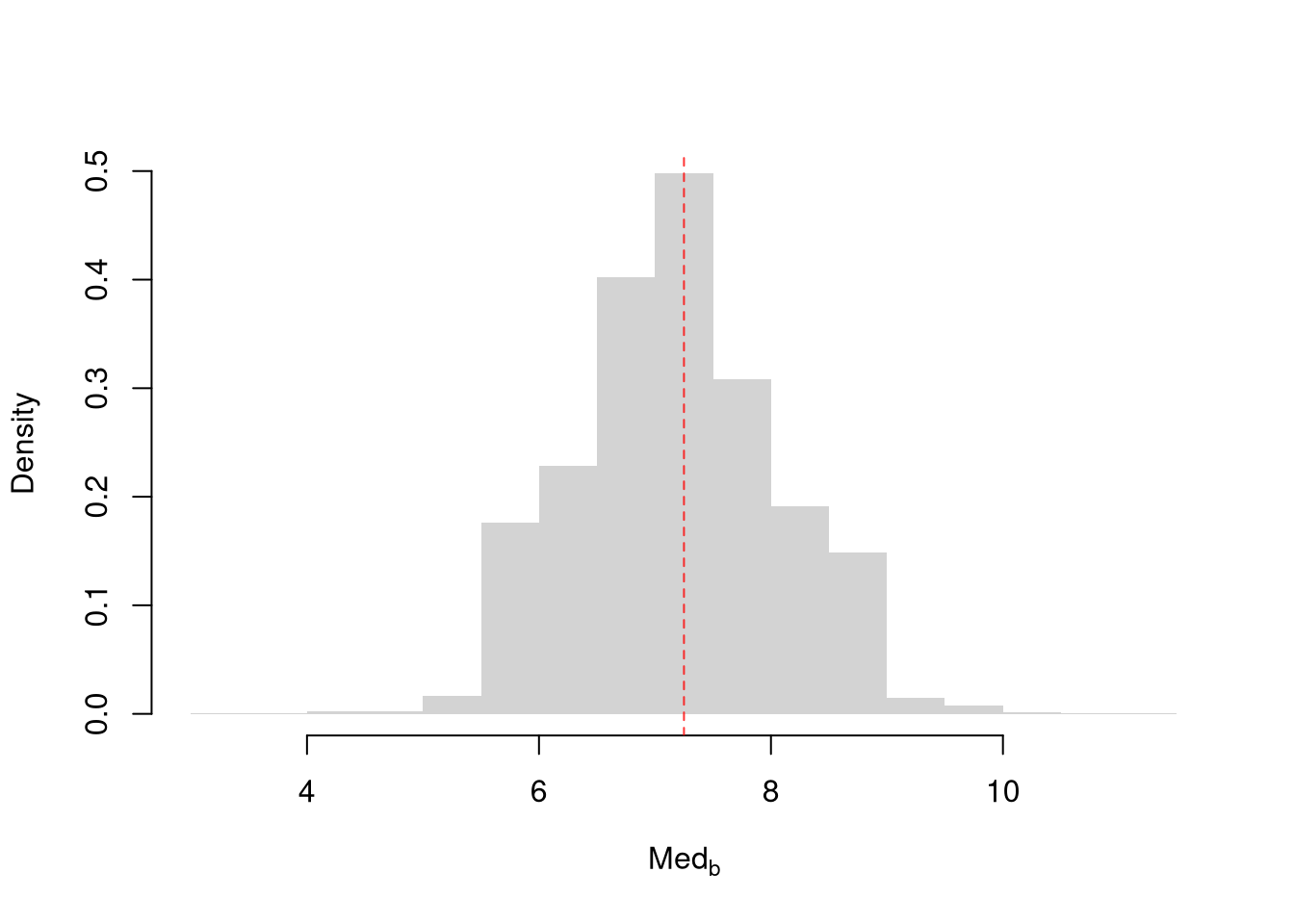

med <- quantile(sample_dat, prob=0.5)

# Bootstrap estimates

bootstrap_stat <- rep(NA, 9999)

for(b in seq_along(bootstrap_stat)){

boot_id <- sample(n, replace=TRUE)

dat_b <- sample_dat[boot_id] # c.f. jackknife

stat_b <- quantile(dat_b, prob=0.5)

bootstrap_stat[b] <- stat_b

}

hist(bootstrap_stat, breaks=25,

border=NA, freq=FALSE,

main=NA, xlab=expression(Med[b]))

abline(v=med, col=rgb(1, 0, 0, .8), lty=2)

This means we can compute bootstrap SEs for other statistics, too.

To generate a random variable from known distributions, you can use some type of physical machine. E.g., you can roll a fair die to generate Discrete Uniform data or you can roll weighted die to generate Categorical data.

There are also several ways to computationally generate random variables from a probability distribution. Perhaps the most common one is inverse sampling. To generate a random variable using inverse sampling, first sample \(p\) from a uniform distribution and then find the associated quantile quantile function \(\hat{F}^{-1}(p)\).2

You can generate a random variable from a known empirical distribution. Inverse sampling randomly selects observations from the dataset with equal probabilities. To implement this, we

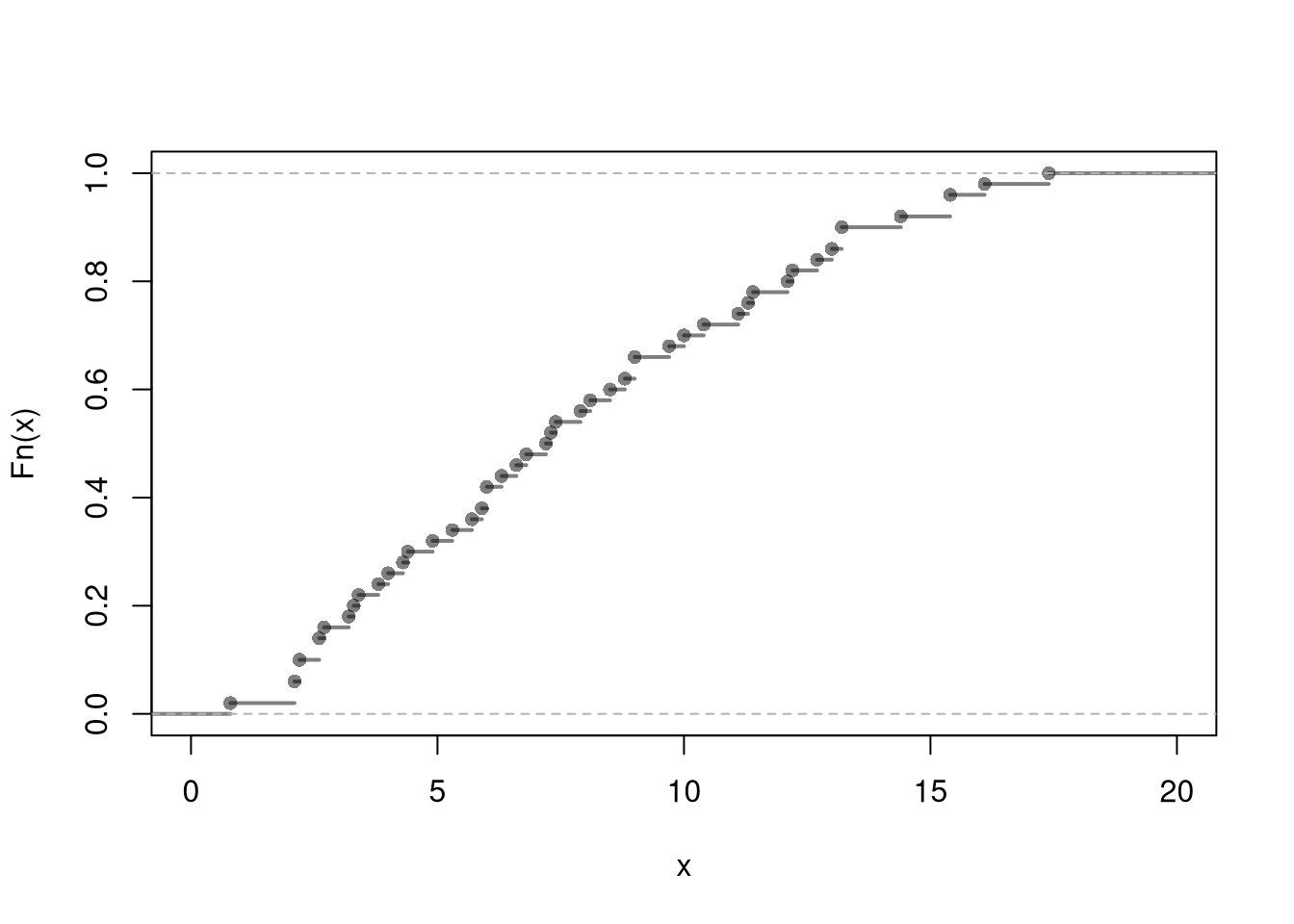

Here is an example of generating random murder rates for US states.

# Empirical Distribution

X <- USArrests[, 'Murder']

FX_hat <- ecdf(X)

plot(FX_hat, lwd=2, xlim=c(0, 20),

pch=16, col=grey(0, .5), main=NA)

# Generating random variables via inverse ECDF

p <- runif(3000) ## Multiple Draws

QX_hat <- quantile(FX_hat, p, type=1)

QX_hat[c(1, 2, 3)]

## 10.828560451% 86.047868826% 60.564645566%

## 2.6 13.2 8.8

## Can also do directly from the data

QX_hat <- quantile(X, p, type=1)

QX_hat[c(1, 2, 3)]

## 10.828560451% 86.047868826% 60.564645566%

## 2.6 13.2 8.8If you know the distribution function that generates the data, then you can derive the quantile function and do inverse sampling. That is how computers generate random data from a distribution.

# 4 random data points from 3 different distributions

qunif(4)

## [1] NaN

qexp(4)

## [1] NaN

qnorm(4)

## [1] NaNHere is an in-depth example of the Dagum distribution. The distribution function is \(F(x)=(1+(x/b)^{-a})^{-c}\). For a given probability \(p\), we can then solve for the quantile as \[F^{-1}(p)=\frac{ b p^{\frac{1}{ac}} }{(1-p^{1/c})^{1/a}}\]. Afterwhich, we sample \(p\) from a uniform distribution and then find the associated quantile.

# Theoretical Quantile Function (from VGAM::qdagum)

qdagum <- function(p, scale.b=1, shape1.a, shape2.c) {

# Quantile function (theoretically derived from the CDF)

ans <- scale.b * (expm1(-log(p) / shape2.c))^(-1 / shape1.a)

# Special known cases

ans[p == 0] <- 0

ans[p == 1] <- Inf

# Safety Checks

ans[p < 0] <- NaN

ans[p > 1] <- NaN

if(scale.b <= 0 | shape1.a <= 0 | shape2.c <= 0){ ans <- ans*NaN }

# Return

return(ans)

}

# Generate Random Variables (VGAM::rdagum)

rdagum <-function(n, scale.b=1, shape1.a, shape2.c){

p <- runif(n) # generate random probabilities

x <- qdagum(p, scale.b=scale.b, shape1.a=shape1.a, shape2.c=shape2.c) #find the inverses

return(x)

}

# Example

set.seed(123)

X <- rdagum(3000, 1, 3, 1)

X[c(1, 2, 3)]

## [1] 0.7390476 1.5499868 0.8845006Comment the script you wrote for this chapter, then restart R and check that it runs from a clean session, then check the script with AI as explained in Working with AI. Write three sentences from memory on the main statistical idea of this chapter, and ask the assistant what is wrong, vague, or missing. Finish with your own questions about whatever you found hardest.

In your own words, explain the difference between the standard deviation of a sample and the standard error of the sample mean. Why does the standard error decrease as \(n\) grows, while the standard deviation does not necessarily change?

Consider a population of four students with ages \(\{18, 20, 22, 24\}\). List all possible simple random samples of size \(n=2\) (without replacement). Compute the sample mean for each. Then compute the mean and standard deviation of those sample means. Verify that the mean of the sample means equals the population mean.

Load USArrests in R and extract the UrbanPop column. Write a bootstrap loop with \(B=5000\) resamples to estimate the standard error of the median. That is, for each resample draw n observations with replacement, compute the median, store it, and then compute sd of the stored medians. Compare this bootstrap standard error to the bootstrap standard error of the mean from the same data.

This chapter introduced sampling distributions (how a statistic varies across samples), the Law of Large Numbers and Central Limit Theorem that govern the sample mean, and the jackknife and bootstrap methods that approximate sampling variability from a single dataset, summarized by the standard error. The four-student example tied these ideas to concrete numbers: from ages \(\{18, 20, 22, 24\}\) there are six possible samples of size \(n=2\) giving six sample means \(\{19, 20, 21, 21, 22, 23\}\) centered on the population mean \(21\), and the histogram of those six values is the sampling distribution of \(\hat{M}\). In the next chapter we formalize the link between sample statistics and population parameters: estimate, estimator, and parameter.